Nuclear Power in the USA

- The USA is the world's largest producer of nuclear power, accounting for about 30% of worldwide generation of nuclear electricity.

- The country's nuclear reactors produced 816 TWh in 2024, 18% of total electrical output.

- Vogtle 3 was connected to the grid in April 2023, followed by unit 4 in March 2024.

- The Inflation Reduction Act was signed into law in August 2022. The Act provides support for existing and new nuclear development through investment and tax incentives for both large existing nuclear plants and newer advanced reactors, as well as high-assay low enriched uranium (HALEU) and hydrogen production.

- Targets to quadruple US nuclear capacity (to 400 GWe) by 2050 and to deploy advanced reactors in the near term were set by the administration in 2025.

Reactors

Construction

Shutdown

Electricity sector

Total generation (in 2024): 4596 TWh

Generation mix: natural gas 1929 TWh (42%); nuclear 816 TWh (18%); coal 721 TWh (16%); wind 457 TWh (10%); hydro 268 TWh (6%); solar 275 TWh (6%); biofuels & waste 59.4 TWh (1%); oil 30.7 TWh; geothermal 18.5 TWh.

Import/export balance: 13.8 TWh net import (33.3 TWh imports; 19.4 TWh exports)

Total consumption: 4034 TWh

Per capita consumption: c. 11,900 kWh in 2024

Source: International Energy Agency and The World Bank. Data for year 2024.

Nuclear power industry

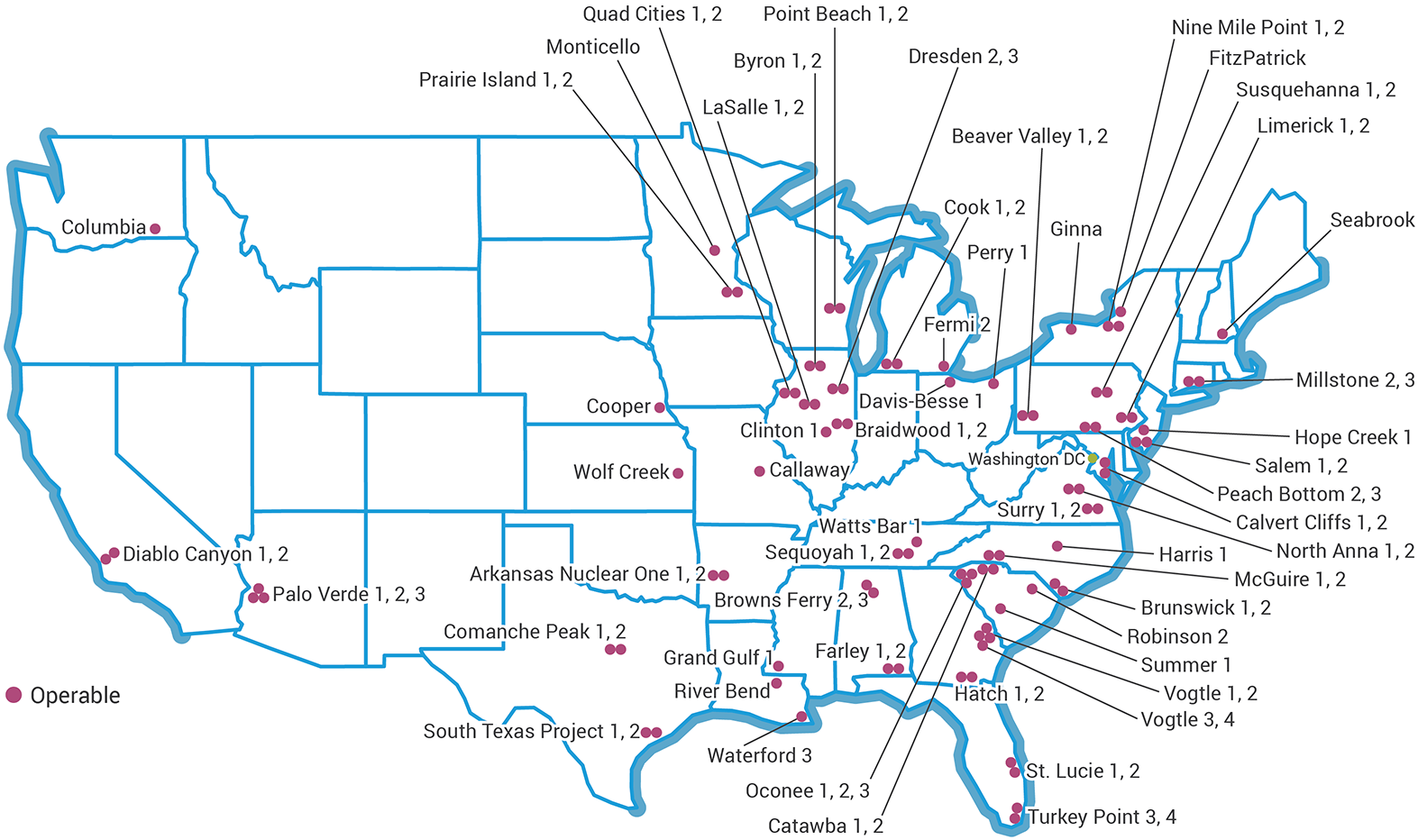

Operable reactors in the USA

A table of operable plants in the USA is available as an appendix to this page.

Nuclear power plays a major role in electricity provision across the country. The US fleet is operated across 28 different states. Since 2001 these plants have achieved an average capacity factor of over 90%. The average capacity factor has risen from 50% in the early 1970s, to 70% in 1991, and it passed 90% in 2002, remaining at around this level since. In 2019 it was a record 94%. The industry invests about $8 billion per year in maintenance and upgrades of the plants.

Nuclear plants generate nearly 20% of the country's electricity overall and about 55% of its carbon‐free electricity.

Since about 2010 sustained low natural gas prices dampened plans for new nuclear capacity (see section on New nuclear capacity below). However, in August 2022 the Inflation Reduction Act was passed by the US House of Representatives and later that month signed into law by President Joe Biden. The energy provisions in the Act outline support for existing and new nuclear development through investment and tax incentives for both large existing nuclear plants and newer advanced reactors, as well as HALEU and hydrogen production.

Later, in May 2025 US President Donald Trump signed a series of executive orders designed to stimulate growth in the industry with the aim of quadrupling capacity by 2050 (see section on Presidential executive orders, May 2025 below).

Nuclear industry development

The USA was a pioneer of nuclear power development.a Westinghouse designed the first fully commercial pressurized water reactor (PWR), a unit of 250 MWe capacity, Yankee Rowe, which started up in 1960 and operated to 1992. Meanwhile the boiling water reactor (BWR) was developed by the Argonne National Laboratory, and the first commercial plant, Dresden 1 (250 MWe) designed by General Electric, was started up in 1960. A prototype BWR, Vallecitos, ran from 1957 to 1963.

By the end of the 1960s, orders were being placed for PWR and BWR reactor units of more than 1000 MWe capacity, and a major construction program got under way. These remain practically the only types built commercially in the USA.b

Almost all the US nuclear generating capacity comes from reactors built between 1967 and 1990. Until 2013 there had been no new construction starts since 1977, largely because for a number of years gas generation was considered more economically attractive and because construction during the 1970s and 1980s had frequently been delayed.

Nuclear developments in USA suffered a major setback after the 1979 Three Mile Island accident, though that actually validated the very conservative design principles of Western reactors, and no-one was injured or exposed to harmful radiation. Many orders and projects were cancelled or suspended, and the nuclear construction industry went into the doldrums for two decades. Nevertheless, by 1990 over 100 commercial power reactors had been commissioned.

A further PWR – Watts Bar 2 – started up in 2016 following Tennessee Valley Authority's (TVA's) decision in 2007 to complete the construction of the unit, and Vogtle 3&4 were connected to the grid in 2023 and 2024 respectively.

Most reactors were built by regulated utilities, often state-based, which meant that they put the capital cost (whatever it turned out to be after, for example, delays) into their rate base and amortized it against power sales. Their consumers bore the risk and paid the capital cost. (With electricity deregulation in some states, the shareholders bear any risk of capital overruns and power is sold into competitive markets.)

Despite a near halt in new construction for more than 30 years, US reliance on nuclear power has grown. In 1980, nuclear plants produced 251 TWh, accounting for 11% of the country's electricity generation. In 2023 output was 779 TWh providing about 19% of electricity. Much of the increase came from the 47 reactors, all approved for construction before 1977, that came online in the late 1970s and 1980s, more than doubling US nuclear generation capacity. The US nuclear industry has also achieved remarkable gains in power plant utilization through improved refuelling, maintenance and safety systems at existing plants. Average nuclear generation costs have come down from $52.83/MWh (in 2023 dollars) in 2012 to $31.76/MWh in 2023. This 40% reduction in nuclear generating costs since 2012 has been driven by: a 41% decrease in fuel costs; a 51% decrease in capital expenditures; and a 33% decrease in operating costs.9

Operationally, from the 1970s the US nuclear industry dramatically improved its safety and operational performance, and by the turn of the century it was among world leaders, with average net capacity factor over 90%.

This performance was achieved as the US industry continued deregulation, begun with passage of the Energy Policy Act in 1992. Changes accelerated after 1998, including mergers and acquisitions affecting the ownership and management of nuclear power plants.

Reactor lifetime extensions and regulation

The Nuclear Regulatory Commission (NRC) is the government agency established in 1974 to be responsible for regulation of the nuclear industry, notably reactors, fuel cycle facilities, materials and waste (as well as other civil uses of nuclear material).

In an historic move, the NRC in March 2000 renewed the operating licences of the two-unit Calvert Cliffs nuclear power plant for an additional 20 years. In March 2019 the NRC renewed the licence for Seabrook, extending the unit’s operation by 20 years to 2050. This took the number of US power reactors that have renewed their licences to 94, several of which have since shut down. Hence, almost all of the US power reactors are likely to be licensed to operate for 60 years, with owners undertaking major capital works to upgrade them at around 30-40 years. The licence renewal process typically costs $16-25 million, and the procedures for such renewals, with public meetings and thorough safety review, are exhaustive.

The original 40-year licences were always intended to be renewed in 20-year increments, as the 40-year period was more to do with amortization of capital rather than implying that reactors were designed for only that operational lifespan. It was also a conservative measure, and experience since has identified life-limiting factors and addressed them. The NRC is now considering applications for the extension of operating licences beyond 60 out to 80 years, with its subsequent licence renewal (SLR) programme. As of June 2026:

- Reactors approved (to 80 years): Turkey Point 3&4, Peach Bottom 2&3, Surry 1&2, North Anna 1&2, Monticello, Oconee 1-3, Virgil C. Summer 1, Point Beach 1&2, Browns Ferry 1-3, Dresden 2&3, St. Lucie 1&2, H.B. Robinson 2, Hatch 1&2.

- Reactors under review: Edwin I, Nine Mile Point 1.

In March 2026 Arizona Public Service announced its intention to seek subsequent licence renewal for all three Palo Verde units, with a notice of intent for the application planned for late 2027.

The licence extensions to 60 years and beyond meant that major mid-life refurbishment, such as replacement of steam generators and upgrades of instrument and control systems, could be justified. While active plant components such as pumps and valves are under continuous scrutiny for operability, passive components need to be assessed for ageing which may have weakened them. There are R&D programmes focusing on this run by the Department of Energy (DOE), Electric Power Research Institute (EPRI), and American Society of Mechanical Engineers (ASME).

The NRC's reactor oversight and assessment process yields publicly-accessible information on the performance of plants in 19 key areas (14 indicators on plant safety, two on radiation safety and three on security). Performance against each indicator is reported quarterly on the NRC website according to whether it is normal, attracting regulatory oversight, provoking regulatory action, or unacceptable (in which case the plant would probably be shut down).

On the industry side, the Institute of Nuclear Power Operations (INPO) was formed after the Three Mile Island accident in 1979, to establish standards of performance against which individual plants could be regularly measured. An inspection of each member plant is typically performed every 18 to 24 months.

Following the accident at Japan's Fukushima nuclear plant in March 2011, which was exacerbated by inadequate outside assistance to the flooded reactors, the US nuclear industry set up the 'FLEX' accident response strategy. It has 61 centres across the country and two national centres which together provide the capacity to respond to nuclear power plant accidents anywhere in the country within 24 hours.

In September 2025 the USA and UK signed the Technology Prosperity Deal that deepens collaboration between the NRC and the UK’s Office for Nuclear Regulation (ONR) and Environment Agency to support the completion of reactor design reviews within two years and site approvals within one year.

New nuclear capacity

From 1992 to 2005, some 270,000 MWe of new gas-fired plant was built, and only 14,000 MWe of new nuclear and coal-fired capacity came online. But coal and nuclear supplied almost 70% of US electricity at the time and provided price stability. When investment in these two technologies almost disappeared, unsustainable demands were placed on gas supplies and prices quadrupled, forcing large industrial users of it offshore and pushing gas-fired electricity costs towards 10 ¢/kWh. However, due to technological advances (in particular, horizontal drilling techniques) in shale gas fracking in the 2000s, costs became much lower.

The reason for investment being predominantly in gas-fired plant was that it offered the lowest investment risk. Several uncertainties inhibited investment in capital-intensive new coal and nuclear technologies. The average age of US nuclear plants is over 40 years, and major investment is also required in transmission infrastructure. This creates an energy investment crisis which is recognized in Washington, along with an increasing bipartisan consensus on the strategic importance and clean air benefits of nuclear power in the energy mix.

In 2002, the Department of Energy (DOE) launched its Nuclear Power 2010 (NP2010) programme to reinvigorate the US nuclear power industry through identifying sites, demonstrating untested regulatory processes and developing advanced nuclear technologies.

As part of the NP2010 initiative, in 2003, the Department of Energy (DOE) called for combined construction and operating licence (COL) proposals on the basis that it would fund up to half the cost of any accepted.

Several industry consortia were created for the purpose of preparing COL applications for new reactors. Although few of these projects went ahead, the secured COLs have a validity spanning 40 years from the date of issue, with the possibility of extension for a further 20 years.

Further information is given in Nuclear Power in the USA Appendix 3: COL Applications.

The Energy Policy Act (EPA) of 2005 provided a much-needed stimulus for investment in electricity infrastructure including nuclear power.

The EPA introduced a production tax credit (PTC) of 1.8 cents per kilowatt hour of electricity produced by new nuclear plants in their first eight years of operation. The tax credit was available only for the first 6000 MWe of new nuclear capacity and could not be claimed until electricity generation commenced.

Under the terms of the EPA, to qualify for the nuclear PTC, a plant needed to be in service on or before 31 December 2020, and the maximum value of the nuclear PTC was $6 billion over eight years (or $750 million per year). However in February 2018, an extension to the PTC was passed by the US Senate and Congress that allowed reactors entering service after 31 December 2020 to qualify for the tax credits, and allowed the US Energy Secretary to allocate credit for up to 6000 MWe of new nuclear capacity which enters service after 1 January 2021.

The Inflation Reduction Act of 2022 further extended the PTC, offering a credit of 1.5 cents per kilowatt hour for certain existing nuclear plants and plants placed in service after 31 December 2024. It runs through 2031 (shortened from 2032 by the One Big Beautiful Bill Act of July 2025, which also introduced new clean electricity tax credits expiring in 2034 and replaced the DOE’s loan programmes with the Energy Dominance Financing programme). The credit, which is indexed to inflation and dependent on certain wage requirements being met, gradually declines as power prices rise above 2.5 cents per kilowatt hour.

For further discussion see information page on US Nuclear Power Policy.

New reactor construction got under way from 2012, with two units at the Vogtle nuclear power plant, and two units at the Summer nuclear power plant.*

* The project at Summer was subsequently cancelled.

Continued low gas prices have since depressed the prospects for commitment to further construction, and it is generally considered that natural gas prices need to recover to $8/GJ or /MMBtu before there is renewed confidence in deregulated states. In regulated states, a longer-term outlook is possible. Small modular reactors provide possible relief from major upfront finance burdens, but many of these designs are some way off having design certification from the NRC.

There are three regulatory initiatives that have enhanced the prospects of building new plants. First is the design certification process, second is provision for early site permits (ESPs) and third is the combined construction and operating licence (COL) process (‘Part 52’ of Title 10 of the Code of Federal Regulations) as an alternative to the ‘Part 50’ two-step process of construction permit followed by operating licence. All have some costs shared by the DOE.

A COL application under 10 CFR Part 52 may reference a design certification and/or an ESP. This allows the issues resolved during the design certification and ESP processes to be precluded from reconsideration during the COL licensing process.

Government support

Presidential executive orders, May 2025

In May 2025 US President Donald Trump signed a series of executive orders titled Reinvigorating the Nuclear Industrial Base, Reforming Nuclear Reactor Testing at the Department of Energy and Ordering the Reform of the Nuclear Regulatory Commission with the goal of "re-establishing the United States as the global leader in nuclear energy.” The aim of the executive orders is to increase capacity from 100 GWe to 400 GWe by 2050, including the Department of Energy (DOE) prioritizing work "with the nuclear energy industry to facilitate 5 gigawatts of power uprates to existing nuclear reactors and have 10 new large reactors with complete designs under construction by 2030." In March 2026 the DOE launched the UPRISE (Utility Power Reactor Incremental Scaling Effort) programme, with the Office of Energy Dominance Financing offering up to 80% financing for uprate projects.

The executive order Reinvigorating the Nuclear Industrial Base states:

"Swift and decisive action is required to jumpstart America’s nuclear energy industrial base and ensure our national and economic security by increasing fuel availability and production, securing civil nuclear supply chains, improving the efficiency with which advanced nuclear reactors are licensed, and preparing our workforce to establish America’s energy dominance and accelerate our path towards a more secure and independent energy future."

The Reforming Nuclear Reactor Testing at the Department of Energy executive order seeks to maximize the use of the DOE’s authority to approve reactor construction and operation on its sites, which can be used to demonstrate reactor designs independently of the NRC’s processes.

The executive order set a target to build and achieve criticality with at least three innovative reactor designs at DOE sites by July 2026. Subsequent shortlisting by the DOE identified 10 companies that it would work with: Aalo Atomics, Antares Nuclear, Atomic Alchemy, Deep Fission, Last Energy, Oklo, Natura Resources, Radiant Industries, Terrestrial Energy, and Valar Atomics. In November 2025, Valar Atomics became the first company in the programme to achieve criticality at its NOVA Core located at the National Criticality Experiments Research Center (NCERC) of Los Alamos National Laboratory (LANL). In March 2026 the DOE established the Launch Pad programme to provide infrastructure and regulatory support for advanced reactor and fuel cycle facility demonstrations at Idaho National Laboratory and elsewhere.

The executive order Ordering the Reform of the Nuclear Regulatory Commission says:

"Instead of efficiently promoting safe, abundant nuclear energy, the NRC has instead tried to insulate Americans from the most remote risks without appropriate regard for the severe domestic and geopolitical costs of such risk aversion."

In February 2014 the NRC had said that its most optimistic scenario for awarding design certification for new small reactors was 41 months, assuming they were light water types (PWR or BWR). The executive order obviously intends to spur a significant acceleration of this and other new build licensing activities, although without specifying how.

US government and Westinghouse

In October 2025 the US government announced a $80 billion strategic partnership with Westinghouse Electric Company and its owners Brookfield Asset Management and Cameco Corporation to deploy a fleet of AP1000 and AP300 reactors across the USA. The partnership includes government-arranged financing and facilitated permitting, with the government receiving a 20% participation interest in cash distributions above $7.5 billion. A March 2026 study by PricewaterhouseCoopers, commissioned by Westinghouse, Brookfield and Cameco, estimated that a ten-unit AP1000 fleet in the USA would generate $92.8 billion in GDP and support 44,300 jobs annually during the 13-year construction phase, and $1.03 trillion in cumulative GDP over 80 years of operation.

Big tech investment

Since about 2023 the world’s largest technology companies have made a series of investments in nuclear energy in the United States, both through power purchase/offtake agreements and direct investments/development agreements.

- May 2023 – Microsoft signs PPA from Helion’s planned fusion plant.

- September 2024 – Microsoft signs 20-year PPA supporting restart of Three Mile Island 1 (see below).

- October 2024 – Google signs deal with Kairos Power to purchase energy from multiple SMRs.

- October 2024 – Amazon invests $500 million in X-energy.

- December 2024 – Switch signs non-binding agreement with Oklo to purchase energy from 12 GWe of Oklo Aurora powerhouse projects through 2044.

- June 2025 – Amazon signs PPA running to 2042 with Talen’s Susquehanna nuclear power plant.

- June 2025 – Google signs PPA for 200 MWe from Commonwealth Fusion Systems' planned plant in Chesterfield County, Virginia.

- January 2026 – Meta signs 20-year PPA for 2176 MWe from the Perry and Davis-Besse plants in Ohio; plus the purchase of energy from uprates at those two plants and the Beaver Valley plant in Pennsylvania.

- January 2026 – Meta agrees funding to support deployment of two Terrapower Natrium sodium fast reactors (2x345 MWe) with delivery from 2032, plus the rights for energy from up to six other Natrium units targeted for delivery by 2035.

- January 2026 – Meta agrees to prepay for power and provide funding to advance Oklo’s project to develop a 1.2 GWe power campus in Pike County, Ohio.

New reactor licensing

There are three regulatory initiatives that have enhanced the prospects of building new plants. First is the design certification process, second is provision for early site permits (ESPs) and third is the combined construction and operating licence (COL) process (‘Part 52’ of Title 10 of the Code of Federal Regulations) as an alternative to the ‘Part 50’ two-step process of construction permit followed by operating licence. All have some costs shared by the DOE.

A COL application under 10 CFR Part 52 may reference a design certification and/or an ESP. This allows the issues resolved during the design certification and ESP processes to be precluded from reconsideration during the COL licensing process.

Design certification

As part of the effort to increase US generating capacity, the government and industry have worked closely on design certification for advanced Generation III reactors. Design certification by the Nuclear Regulatory Commission (NRC) means that, after a thorough examination of compliance with safety requirements, a generic type of reactor (say, a Westinghouse AP1000) can be built anywhere in the USA, only having to go through site-specific licensing procedures and obtaining a combined construction and operating licence (see below) before construction can begin. In September 2025 the duration of design certifications was revised to 40 years (previously 15 years).

Designs now having US design certification are:

- The Westinghouse AP1000, which is the first Generation III+ reactor to receive certificationc. It is a scaled-up version of the Westinghouse AP600 which was certified earlier. It has a modular design to reduce construction time to 36 months. Four are in operation in China, as well as two in the USA.

- The GE Hitachi advanced boiling water reactor (ABWR) of 1300-1500 MWe. Several ABWRs are now in operation and under construction in Japan. Some of these have had Toshiba involved in the construction, and more recently it has been Toshiba that promoted the design most strongly in the USA.d Both the Toshiba and the GE Hitachi versions needed to have their design certification renewed from 2012. Toshiba withdrew its design certification renewal application in mid-2016.

- GE Hitachi's Economic Simplified BWR (ESBWR) of 1600 MWe gross with passive safety features, developed from the ABWR. GE Hitachi submitted the application in August 2005, design approval was notified in March 2011, and design certification was in September 2014. The first combined construction and operating licence (COL) with it was awarded for Fermi 3 in May 2015 and the second for North Anna 3 in June 2017.

- The Korean APR-1400 reactor, which is operating in South Korea since 2016 and in the United Arab Emirates since 2020. Korea Hydro & Nuclear Power submitted a design certification application to the NRC in October 2013 and the revised submission was accepted by the NRC in March 2015. The final safety report was published in September 2018 and design certification was given in May 2019.

- An uprated 250 MWt (77 MWe gross) NuScale Power Module design was accepted by the NRC in July 2023 and approved in May 2025. This design is an uprated version of the 160 MWt (50 MWe gross) NuScale Power Module design, which was earlier accepted for review by the NRC in March 2017 and approved in September 2020. A reactor building would contain up to 12 of the 77 MWe NuScale Power Modules. The design comprises a reactor core, pressurizer and two steam generators integrated within a reactor pressure vessel and housed in a compact steel containment vessel. The uprated design is the basic unit of NuScale’s VOYGR plants: VOYGR-12 (924 MWe), VOYGR-6 (462 MWe) and VOYGR-4 (308 MWe). The initial plant was planned to be the UAMPS Carbon Free Power Project, a VOYGR-6 plant at the Idaho National Laboratory, which would be owned by Utah Associated Municipal Power Systems (UAMPS).

Reactor designs formerly undergoing US design certification:

- The US Evolutionary Power Reactor (US EPR), an adaptation of Areva's EPR to make the European design consistent with US electricity frequencies. The main development of the type was to be through UniStar Nuclear Energy, but other US proposals also involved it. The application was submitted in December 2007 and the design certification rule was expected after mid-2015, with delays due to the complexity of digital instrumentation and control systems. Areva then delayed the NRC schedule and in March 2015 indefinitely suspended the application. EPRs have been built in Taishan in China, as well as Finland and France. Two units are under construction in the UK at Hinkley Point C.

- The Mitsubishi US-APWR, a 1700 MWe design developed from that for a 1538 MWe reactor planned for Tsuruga in Japan. The application was submitted in December 2007 and certification was expected to be completed in February 2016, but Mitsubishi delayed the NRC schedule for “several years”. European certification for the almost identical EU-APWR was granted in October 2014. Two US-APWR reactors were proposed in the Luminant-Mitsubishi application for Comanche Peak, but Mitsubishi has withdrawn from this project.

Several designs of small modular reactors (SMRs) are proceeding with pre-application activities towards NRC design certification application, including:

- GE Hitachi Nuclear Energy submitted licensing documentation to the NRC in December 2019 for the BWRX-300. The company said the design "leverages the design and licensing basis of the NRC-certified ESBWR" and that it "represents the simplest, yet most innovative BWR design since GE began developing nuclear reactors in 1955."

- Holtec International announced in November 2020 that it had commenced licensing procedures with the NRC. A demonstration unit of the 160 MWe Holtec SMR-160 PWR (with external steam generator) had been proposed at the Savannah River Site with DOE support. In December 2023 Holtec announced a new plan to build its first two SMR units – using the 300 MWe version of its SMR design, the SMR-300 – at its Palisades nuclear plant in Michigan. Holtec said it plans to file a construction permit application with the NRC by 2026 and has a target commissioning date for the first SMR-300 in the mid-2030s.

- In March 2025, Switzerland-based Deep Atomic entered the pre-application process for design certification of its MK60 design. The MK60 is a PWR with 60 MWe capacity that also provides 60 MW cooling capacity, which can support the thermal management requirements of a large data centre, according to Deep Atomic.

A fuller account of new reactor designs, including those certified but not marketed in the USA, is in the information page on Advanced Nuclear Power Reactors, or for the small modular reactors, in the page on Small Nuclear Power Reactors.

Early site permit

Early site permits facilitate a utility or project developer to engage the NRC on the suitability of a site to host a nuclear power plant in advance of making firm decisions on either reactor design or whether to proceed with nuclear build. If granted, ESPs are valid for 10 to 20 years from the date of issue, with the possibility of extension by a further 10 to 20 years.

The ESP programme was launched in 2001, attracting four applicants: Exelon, Entergy, Dominion and Southern, for Clinton, Grand Gulf, North Anna and Vogtle sites respectively – all sites then with operating nuclear plants but room for more.

In March 2007, Exelon was awarded the first ESP for its Clinton plant in Illinois, after 41 months' processing by the NRC and public review. The NRC then awarded ESPs to Entergy for its Grand Gulf site, Dominion for North Anna, and Southern for Vogtle. No plant type is normally specified with an ESP application, but the site is declared suitable on safety, environmental and related grounds for a new nuclear power plant. The last three of these 2001 ESPs were replaced by COL applications.

In March 2010, Exelon applied for an ESP for its Victoria County, Texas, site and withdrew the COL application for that project. In 2012 it withdrew the ESP application. PSEG Nuclear lodged an application for an ESP for a new reactor at its Salem/Hope Creek site on the Delaware River in New Jersey in May 2010, and this was granted in May 2016.

The seventh ESP application was for small reactors. In May 2016 Tennessee Valley Authority (TVA) submitted an ESP application to the NRC for up to 800 MWe total generating capacity across multiple small reactors at Clinch River. The application was based on a plant parameter envelope encompassing the light-water SMRs currently under development in the USA by BWX Technologies, Holtec, NuScale Power and Westinghouse. It envisaged that the emergency planning zone need extend only to the site boundary. The ESP, supported by the DOE, was issued in December 2019.

In January 2026 Duke Energy applied for an ESP for a site near the 2200 MWe Belews Creek power plant in North Carolina, which is co-fired by gas and coal and is slated for retirement in the late 2030s. Although the ESP process is technology-neutral, Duke said that it was not considering large light water reactors but instead a range of small and advanced reactors.

Site use permits can be awarded by the DOE for its sites. In December 2019 Oklo received a site use permit for an Aurora reactor to be built at Idaho National Laboratory.

Vogtle 3&4

In April 2008, Georgia Power signed an EPC contract with Westinghouse and The Shaw Group (now CB&I) consortium for two 1200 MWe Westinghouse AP1000 reactors which will be licensed and operated by Southern Nuclear Operating Company (SNOC). Both Georgia Power and SNOC are subsidiaries of Southern Company. JSW in Japan sent forged components to Doosan in South Korea for fabrication. The COL was issued by the NRC in February 2012. Construction start (first concrete) was delayed to late 2012, and then to March 2013, after NRC issued a licence amendment allowing use of a higher-strength concrete that permits the company to pour the foundation of the new reactors without making additional modifications to reinforcing steel bar. At that point ten million working hours had been invested on the site. Shaw (now CB&I) agreed with China's State Nuclear Power Technology Corporation (SNPTC) to deploy engineers with experience in building China's AP1000 units to provide technical support. Following early delays, construction of unit 3 started in March 2013 and unit 4 in November. Fluor joined the project as construction manager in January 2016, taking over part of the CB&I role, and in January 2017 Bechtel became involved with the nuclear islands. The units were initially expected online late in 2019 and September 2020. It is a regulated plant, with guaranteed operational cost recovery.

Reactor pressure vessels and steam generators are from Doosan in South Korea.

Georgia Power as 45.7% owner reduced its earlier cost estimate for building its share of the new plant from $6.4 billion to $6.1 billion as a result of being able to recover financing costs from customers during construction, but this increased to $6.2 billion in 2012 due to delays. Over the life of the plant, the utility's customers will save about $1 billion through federal loan guarantees, production tax credits and the early recovery of financing costs in the rate base. The Georgia Public Service Commission in February 2013 approved Georgia Power's costs for the project and said that the project "remains more economically viable than any other [energy] resource, including a natural gas-fired alternative."

The initial cost estimate for the project was $14 billion. Delays to mid-2014 resulted in a cost increase of $381 million but this was offset by lower interest rates than budgeted. When further delays were announced in January 2015, the company said that cost escalation was about $10 million per month plus financing cost of about $30 million per month. Minority equity in the project is held by Oglethorpe Power (30%), the Municipal Electric Authority of Georgia – MEAG Power (22.7%), and Dalton city (1.6%).

Loan guarantees totalling $3.5 billion were issued to Georgia Power and $3 billion to Oglethorpe Power in 2014. A further $1.8 billion of loan guarantees were issued to three subsidiaries of MEAG Power in June 2015, making a total of $8.3 billion. (Dalton Utilities did not seek a loan guarantee.) In August 2017 Georgia Power, Oglethorpe Power and MEAG sought further loan guarantees to help them complete the project. In September 2017 the DOE announced conditional commitments for further loan guarantees of up to $3.7 billion: $1.67 billion to Georgia Power, $1.6 billion to Oglethorpe Power, and $415 million to three subsidiaries of MEAG Power. (Dalton Utilities again did not apply.) These were granted in March 2019. The DOE said: "Advanced nuclear energy projects like Vogtle are the kind of important energy infrastructure projects that support a reliable and resilient grid, promote economic growth, and strengthen our energy and national security.”

Earlier, in mid-April 2017, Westinghouse said that about $1.5 billion was required to complete the construction of both units, though other estimates are higher. In June Toshiba agreed with the owners that its liability under its 2008 parental guarantee would be capped at $3.68 billion for the completion of the Vogtle units. The sum is part of an $8.9 billion provision in Toshiba’s accounts announced in mid-May, covering all four US reactors.

In mid-May 2017 Georgia Power announced that from June, Southern Nuclear Operating Company (SNOC) would take over project management to complete the Vogtle units, leaving Westinghouse simply as the vendor, though supporting EPC and licensing as well as providing access to intellectual property. Southern said that productivity at the site had improved significantly in 2017, with the reactors now two-thirds complete. SNOC will also be the operator. The company said it would "take all actions necessary to hold Westinghouse and Toshiba accountable for their financial obligations."

After a review of options and contingencies, at the end of August 2017 Georgia Power, supported by the co-owners, recommended to the state public services commission (PSC) that construction of both units should be completed, this being the most economic choice for customers. The total rate impact of the project remains less than originally estimated, it said. The recommendation was unanimously approved by the PSC in December 2017.

At the same time Georgia Power announced it had contracted with Bechtel to manage daily construction efforts under the direction of SNOC. Bechtel has been involved with the project since January, correlated with “a marked increase in productivity” providing “every indication that we can do a better job than Westinghouse alone as we move forward to complete the project." Vogtle 3&4 would begin commercial operation in November 2021 and November 2022 respectively, under a new construction schedule. These dates were reaffirmed by Southern Company in September 2020, at which point construction of the two units was 87% complete. However, in April 2021 Southern Company said it was targeting a December 2021 in-service date for unit 3, and in May 2021 officials told the Georgia Public Service Commission that the likely commercial start date was January 2022. In-service dates were moved to Q3 2022 and Q2 2023 in October 2021, before being moved again in February 2022, to Q1 2023 and Q4 2023.

In August 2022 the NRC granted authorization to Southern Company to load fuel and begin commissioning activities at Vogtle 3. Southern said it was aiming to carry out fuel loading before the end of October 2022.

In January 2023 Georgia Power notified the US Securities and Exchange Commission that Vogtle 3's initial criticality would be delayed after vibrations in the plant's cooling system were found and an issue with a dripping valve was identified during start-up and pre-operational testing. A month later, Southern Company announced that the vibration issue had been remediated and testing had resumed. However, an unexpected issue with flow rates through reactor coolant pumps delayed the schedule.

Unit 3 was connected to the grid on 1 April 2023, and entered commercial operation in July. Fuel loading at unit 4 began in August 2023. In October 2023 a motor fault was discovered in a reactor coolant pump at unit 4, slightly delaying its commercial operation to March 2024. In February 2024 vibrations in the cooling system similar in nature to those experienced during the construction of unit 3 were observed at unit 4. In March 2024 unit 4 was connected to the grid.

Georgia Power (45.7% owner) said it had invested about $4.3 billion in capital costs in the project to June 2017 and in August 2018 announced that it had revised its forecast for the cost of its 45% share of the project up to $8.4 billion. The total price for the project in November 2021 was estimated to be over $28 billion. In May 2022 this increased to $30.34 billion.

Watts Bar 2

While the focus is on new technology, TVA undertook a detailed feasibility study which led to its decision in 2007 to complete unit 2 of its Watts Bar nuclear power plant in Tennessee. The 1165 MWe (net) reactor was expected to start up in October 2012 and come online in 2013 at a cost of about $2.5 billion, but this schedule slipped substantially, with major budget overrun to $4.7 billion. Construction had been suspended in 1985 when 80% complete and (after parts were cannibalized to reduce that figure to 61%) resumed in October 2007 under a still-valid permit. The construction permit was extended to September 2016, and in October 2015 TVA received a 40-year operating licence from the NRC. Grid connection was early in June and commercial operation commenced in October 2016. Its twin, unit 1, started operation in 1996.

Completing Watts Bar 2 utilized an existing asset, thus saving time and cost relative to alternatives for new base-load capacity. It was expected to provide power at 4.4 ¢/kWh, 20-25% less than coal-fired or new nuclear alternatives and 43% less than natural gas. It is a regulated plant, with guaranteed cost recovery.

In 2014, before start-up, TVA ordered four new steam generators for the unit to be installed in 2022 at a cost of $160 million. The early 1980s ones were made of an alloy that is prone to stress corrosion cracking. Those in unit 1 were replaced after nine years of operation, and the vast majority of US PWRs have had replacements.

Nuclear reactor restarts

Palisades

In September 2017 Entergy announced that it would keep its Palisades nuclear plant in Michigan open until 2022. The company had previously announced in December 2016 that it planned to close the 789 MWe net unit in October 2018 due to economic factors in the partly deregulated market. The reactor was shut down in May 2022 and sold to Holtec International in June for decommissioning.

In light of the DOE’s publication of its Civil Nuclear Credit Program – aiming to keep marginal units in deregulated environments online to help accelerate the US energy transition – in September 2022, Holtec international began exploring the possibility of restarting the plant. In November 2022 the DOE rejected Holtec’s application that sought funding under the Civil Nuclear Credit Program to reactivate Palisades.

The following month, Holtec announced plans to launch a second attempt to secure federal funding to restart the unit. In January 2023 the Board of Commissioners of Allegan County, Michigan voted unanimously in favour of Holtec’s bid to obtain federal funding to restart the unit.

In March 2023 Holtec applied for federal funding from the DOE under the Civil Nuclear Credit Program to restart the Palisades plant, which it believes would cost more than $1 billion. In September 2023 a long-term power purchase agreement was agreed between Palisades Energy and Wolverine Power Cooperative. Later that month, Holtec applied to the NRC for reauthorization of power operations at the plant. Also in the same month, Wolverine Power Supply submitted an application for funding through the US Department of Agriculture’s Empowering Rural America (New ERA) $9.7 billion grant and loan initiative that is funded by the Inflation Reduction Act.

In October 2025 new fuel was delivered to the plant. The restart was initially expected by the end of 2025, but was delayed by steam generator tube repairs, with the restart now expected in 2026.

Crane Clean Energy Center (Three Mile Island 1)

Three Mile Island 1 was shut down in September 2019 due to economic challenges (see Electricity Market Challenges, below). Although the unit had been licensed to operate until 2034, Exelon had announced in May 2017 that it would be closed if policy reforms recognising nuclear as a low-carbon electricity producer were not enacted.

The plant’s name was changed to the Crane Clean Energy Centre in 2025. Constellation has signed a 20-year power purchase agreement with Microsoft and intends to bring the unit back into operation in 2028. In September 2025 Constellation said the project was ahead of schedule with commercial operation now expected in 2027.

In November 2025 the DOE issued a $1 billion loan to Constellation to support the restart.

Duane Arnold

The single-unit Duane Arnold plant was licenced to operate until 2034 but owner NextEra opted to close it in 2020 after a major power purchase customer shortened its contract and the plant suffered non-nuclear damage in a major storm. Fuel was removed and placed in dry storage and the plant entered a non-operational status. Duane Arnold’s grid interconnection rights were split up to support a number of prospective solar projects.

However, by 2024 regional increases in demand for continuous clean power caused NextEra to reassess the unit’s economics and begin work to bring it back into operation. In January 2025 NextEra applied to the NRC to restore its operational status. In September 2025 the Federal Energy Regulatory Commission agreed to reconsolidate the unit’s previous interconnection rights. In October 2025 Google signed a 25-year power purchase agreement with NextEra for the plant. In January 2026 Linn County approved rezoning to support the restart, which is expected in early 2029.

Nuclear power reactors restarting

| Site | MWe net | Proponent/utility | Licensing status | Loan guarantee; restart date |

Licence expiration, once restored |

|---|---|---|---|---|---|

| Palisades | 789 | Holtec |

January 2023: Request filed to restore operational status July 2025: Authorized to receive fresh nuclear fuel |

$1.52 billion; 2026 |

March 2031 |

| Crane Clean Energy Center (Three Mile Island 1) |

835 | Constellation | November 2024: Request filed to restore operational status | $1 billion; 2027 | April 2034 |

| Duane Arnold | 615 | NextEra | January 2025: Request filed to restore operational status | early 2029 | February 2034 |

| Subtotal restarting: 2239 MWe | |||||

New reactor plans and proposals

Proposed nuclear reactors

| Site | Technology | MWe gross | Proponent/utility | Licensing status |

|---|---|---|---|---|

| Kemmerer 1, Wyoming | Natrium | 345 | US SFR Owner (a TerraPower subsidiary) | Construction permit application March 2024; issued March 2026. |

| Seadrift, Texas | Xe-100 | 4x80 | X-energy, Long Mott Energy (a Dow subsidiary) | Construction permit application March 2025. |

| Clinch River, Tennessee | BWRX-300 | 1 x 300 | TVA | ESP application May 2016, issued December 2019. Construction permit application April 2025. |

| Adjacent to Columbia Generating Station, Washington | Xe-100 | 12 x 80 | X-energy, Energy Northwest | |

| Palisades, Michigan | SMR-300 | 2 x 300 | Holtec | Partial construction permit application submitted December 2025; accepted for review February 2026. |

| Idaho National Laboratory, Idaho | Aurora | 75 | Oklo | DOE issued site use permit in 2019. In July 2025 Oklo completed a pre-application readiness assessment for Phase 1 of a COL application. |

| Fermi America 1-4, Carson County, Texas | AP1000 | 4 x 1250 | Fermi America | Partial COL application submitted June 2025. |

| Subtotal proposed: 21 small (2600 MWe) and 4 large (5000 MWe) | ||||

Kemmerer 1

In March 2024, TerraPower submitted a construction permit application for a Natrium reactor at Kemmerer in Lincoln County, Wyoming, near PacifiCorp's Naughton coal-fired plant. The construction permit was authorized in March 2026.

The Natrium reactor is based on the GE Hitachi (now GE Vernova Hitachi Nuclear Energy) 345 MWe (840 MWt) PRISM sodium-cooled fast reactor coupled with a molten salt-based energy storage system. The Natrium storage technology allows the system's output to be increased to 500 MWe for five-and-a-half hours.

Terrapower is also constructing a ‘sodium test and fill facility’ nearby to test components for use in the Natrium plant as well as to carry out the initial transfer of sodium to the plant. Construction of this began in June 2024.

TerraPower was one of two reactor developers (the other being X-energy) to receive the first cost-shared awards of $80 million each under the DOE's Advanced Reactor Demonstration Program (ARDP) in October 2020. The aim of the ARDP is to develop, build and operate two advanced reactors within seven years. The DOE said it would invest up to $3.2 billion over this period in the ARDP.

TerraPower announced in October 2022 that construction of a Natrium fuel fabrication facility would commence in 2023 at the Global Nuclear Fuel - Americas site in Wilmington, North Carolina. However, following Russia's invasion of Ukraine, it has not been viable to source high-assay low-enriched uranium (HALEU) from Russia. The Natrium reactor uses metallic HALEU fuel.

In December 2025 the NRC completed its final safety evaluation for TerraPower's construction permit application, one month ahead of schedule. A construction licence was authorized in March 2026, at which time Terrapower said it would begin construction within weeks. The company had previously said it expected to submit an operating licence application for the Kemmerer plant in 2026. Pre-licensing activities have been underway since mid-2021.

Long Mott Energy

A construction permit application for a four-module (4 x 80 MWe) Xe-100 reactor plant at the Long Mott Generating Station in Calhoun County, Texas was submitted in March 2025.

Xe-100 designer X-energy (along with TerraPower, see above) received a cost-shared award of $80 million in October 2020 under the DOE's Advanced Reactor Demonstration Program (ARDP).

The Xe-100 is a helium-cooled pebble-bed HTR of 200 MWt, 80 MWe would use TRISO-coated uranium oxycarbide fuel made from high-assay low-enriched uranium (HALEU). Factory-made units with a 60-year operating lifetime would be transported to the site by road and installed.

X-energy opened a TRISO pilot fuel fabrication facility at Oak Ridge National Laboratory, Tennessee in 2016 and in April 2022 its TRISO-X subsidiary submitted a Category II special nuclear material licence application the TRISO-X Fuel Fabrication Facility, also at Oak Ridge. The NRC expects the licensing review to last until mid-2026. In the meantime, in October 2022, TRISO-X subsidiary commenced construction work on the facility.

The Long Mott facility would provide process heat and electricity to The Dow Chemical Company's Seadrift Operations site. Long Mott Energy is a wholly-owned subsidiary of Dow.

Clinch River

In April 2025, Tennessee Valley Authority (TVA) applied for a construction permit for a BWRX-300 at its Clinch River site in Oak Ridge, Tennessee. The NRC accepted the application for review in July 2025 and expects to complete its 17-month review by December 2026. An early site permit (ESP) for at least two SMRs (up to 800 MWe) at the site was issued in December 2019.

The ESP application did not reference a particular technology, but in February 2013 Babcock & Wilcox signed an agreement with TVA to build up to four 180 MWe mPower units at Clinch River, with design certification application intended to be submitted to the NRC in 2015.

Energy Northwest, Hanford

Energy Northwest commenced pre-application activities in August 2024 for a construction permit application for up to 12 X-energy Xe-100 units on the Department of Energy’s Hanford site, adjacent to Columbia Generating Station in Benton County, Washington. Energy Northwest has selected AtkinsRéalis as technical advisor for licensing and design activities.

In October 2024 X-energy announced $500 million financing from Amazon’s Climate Pledge Fund and Citadel Founder and CEO Ken Griffin, Ares Management, NGP, and the University of Michigan. Amazon and X-energy are developing four units (320 MWe), with the option to increase that project to 12 units and 960 MWe. The facility will be known as the Cascade Advanced Energy Facility.

Palisades SMR-300

Holtec plans to build a 10 GWe fleet of SMR-300 reactors in North America working with Hyundai Engineering & Construction, with the first two deployed at its Palisades site. Under its ‘Mission 2030’ programme announced in February 2025, Holtec plans to have commenced operation of the pair of SMR-300 units as well as restarted the 789 MWe net PWR at Palisades by the end of 2030. Earlier pre-application activities towards a construction licence application on its SMR-160 design were suspended in December 2023. In December 2025 Holtec submitted a partial construction permit application to the NRC for the two SMR-300 units at Palisades.

In December 2025 the US Department of Energy selected Tennessee Valley Authority and Holtec International to each receive $400 million in federal cost-shared funding to support early deployments of advanced light-water small modular reactors. The funding supports TVA's Clinch River BWRX-300 project and Holtec's planned SMR-300 units at Palisades.

INL Aurora

Oklo aims to build its first Aurora Powerhouse reactor at Idaho National Laboratory for which the DOE has issued a site use permit. In March 2025, Oklo announced that it had increased the capacity of the Aurora reactor 'platform' from 50 MWe to 75 MWe, offering a flexible output range of 15-75 MWe. The sodium-cooled fast neutron reactor would use high-assay low-enriched U-Zr metallic fuel.

Oklo states that the design "is informed by a robust foundation of prior US Department of Energy (DOE) demonstrations and operational experience with fast reactor technologies, most notably the Experimental Breeder Reactor-II (EBR-II) and the Fast Flux Test Facility (FFTF)."

Oklo was given the go-ahead to begin site characterization work at INL in November 2024 for its first Aurora unit, and in September 2025 held a groundbreaking ceremony. Earlier, in August 2025 Oklo announced that Kiewit Nuclear Solutions Co will serve as lead constructor supporting the design, procurement, and construction of the Aurora Powerhouse.

In November 2025 the DOE approved the preliminary documented safety analysis for Oklo's Aurora Fuel Fabrication Facility at INL, allowing assembly to begin. Commercial operation is targeted for late 2027 to early 2028.

In March 2026 the DOE approved nuclear safety design agreements for Oklo’s Aurora Powerhouse at INL. Separately, Oklo’s subsidiary Atomic Alchemy obtained an NRC materials licence for its Groves Isotopes Test Reactor in Caldwell County, Texas.

Oklo previously submitted a combined construction and operating licence (COL) application to the NRC in March 2020 to build and operate a 1.5 MWe Aurora fast heatpipe reactor at the INL site. The NRC accepted this application in June 2020 but denied the COL ‘without prejudice’ in January 2022, saying that important information was missing from the application.

The company recommenced pre-licensing activities with the NRC later that year and in July 2025 announced it had completed a pre-application readiness assessment for Phase 1 of a revised COL application based on the 75 MWe design.

Fermi America

In June 2025 Fermi America submitted the first part of its COL application to build four AP1000 reactors in Carson County, Texas, at the President Donald J Trump Advanced Energy and Intelligence Campus, also referred to as Project Matador. The second part of the COL application was submitted in August. The company aims to put the first reactor in operation in 2032, followed by the others in 2034, 2035 and 2036. The NRC accepted the first two parts of the application in September 2025. Fermi America signed agreements with Hyundai Engineering & Construction and other Korean firms to support design and construction of the project.

The NRC accepted the first two parts of the application in September 2025. Fermi America signed agreements with Hyundai Engineering & Construction and other Korean firms to support design and construction of the project.

Hermes 1&2 and KP-FHR

In December 2023 the NRC issued a construction permit to Kairos Power for the Hermes test reactor, a 35 MWt reduced-scale fluoride-salt-cooled high-temperature reactor prototype for Kairos Power’s fluoride salt-cooled high-temperature reactor (KP-FHR).The reactor would use 19.75% enriched tristructural isotropic (TRISO) high assay low enriched uranium (HALEU) fuel particles embedded in a carbon matrix pebble. In January 2026 Kairos finalized a contract with the DOE to receive the requisite HALEU.

The NRC issued a construction permit in December 2023 and first nuclear concrete was poured in May 2025 at the site of the former Oak Ridge Gaseous Diffusion Plant, within the East Tennessee Technology Park in Oak Ridge, Tennessee. In April 2026 the NRC extended the construction permit completion deadline from the end of 2026 to April 2029.

In November 2024 the NRC issued construction permits for Hermes 2, a two-unit (2 x 35 MWt) demonstration facility; groundbreaking was held in April 2026. Each Hermes 2 unit would use an intermediate salt (BeNaF) loop to exchange heat from the primary (FLiBe) salt to a common steam turbine to demonstrate power generation up to 20 MWe. The planned operating lifetimes of the Hermes 2 reactors are 11 years.

Kairos Power’s 320 MWt/140 KP-FHR is also planned to be built at the East Tennessee Technology Park at Oak Ridge, Tennessee. The reactor uses 19.75% enriched TRISO fuel in pebble form with online refuelling and operates at up to 650°C. Secondary circuit salt is ‘solar’ nitrate, feeding a steam generator. It has passive shutdown and decay heat removal.

In October 2024 Google announced a partnership with Kairos Power for up to 500 MWe of KP-FHR capacity by 2035.

Kewaunee

In September 2025 EnergySolutions and WEC Energy announced they were exploring the construction of new nuclear capacity at the Kewaunee nuclear power plant site in Wisconsin. In January 2026 EnergySolutions submitted a notice of intent for a licensing submission regarding Kewaunee, saying it was evaluating applications for an ESP, construction permit or combined licence. EnergySolutions intends to make its submission by June 2028.

A 556 MWe PWR began operation at the site in 1974 and was shut down in 2013 with its owner, Dominion Energy, citing poor economic conditions. Following its shutdown, ownership was transferred to EnergySolutions to decommission the reactor.

Other proposals, suspended or cancelled

In May 2008, South Carolina Electricity & Gas (SCANA subsidiary) and state-owned Santee Cooper signed an EPC contract with Westinghouse and the Shaw Group (now CB&I) consortium for two 1200 MWe Westinghouse AP1000 reactors. The total forecast cost of $9.8 billion included inflation and owners' costs for site preparation, contingencies and project financing, though the last was reduced and the total estimated in April 2012 was $9.2 billion. In October 2014 the cost was estimated at over $11 billion, and in 2015 SCEG amended the EPC contract to choose a fixed price option for completion of the units. In November 2016 the state public service commission agreed for SCEG’s 55% share to be $7.66 billion, excluding financing, with the company’s return on equity reduced to 10.25%. "These delays and related cost increases are principally due to design and fabrication issues associated with the production of submodules used in construction of the units," according to SCANA. Fluor joined the project as construction manager in January 2016, taking over the CB&I role. In February 2017 the anticipated completion dates for the two units were April 2020 and December 2020.

The COL was issued by the NRC at the end of March 2012, and construction of unit 2 commenced in March 2013, with first main concrete. That for unit 3 was in November 2013. (In September 2011 SCEG had started to assemble the containment vessel for the first unit – 43 mm thick, from Chicago Bridge & Iron – and was starting construction on the four low-profile forced-draft cooling towers.) Reactor pressure vessels and steam generators are from Doosan in South Korea. A crane capable of lifting 6800 tonnes is installed onsite, though the heaviest component was 1550 tonnes. SCEG's loan guarantee application was accepted by the DOE and the project was short-listed in May 2009, though nothing has happened since then. It is a regulated plant, with guaranteed operational cost recovery.

In 2014 it was announced that SCEG’s stake in the project would be increased to 60% by acquisition of 5% from Santee Cooper after the plant starts up, for about $500 million, leaving it with 40%. Duke Energy Carolinas had been seeking up to 10% of the project from Santee Cooper, but this plan was dropped in January 2014.

Following Westinghouse filing for Chapter 11 protection from creditors in March 2017, SCANA reviewed the project and initially expected resources from Westinghouse and Toshiba – including a so-called parental guarantee from Toshiba – to be adequate to compensate for the additional costs. These, together with a surety bond and an escrow of AP1000 intellectual property and software, were considered. SCANA and Santee Cooper had intended to take over project management to complete the Summer units, leaving Westinghouse simply as vendor, though supporting EPC and licensing as well as providing access to intellectual property, as with Vogtle. In mid-April Westinghouse told SCANA that about $1.5 billion was required to complete construction of both units – $829 million more than it was entitled to charge under the EPC contract, but less than the liability amount for it and Toshiba for breach of EPC contract. SCE&G and Santee Cooper reached agreement with Westinghouse and Toshiba to settle for $2.168 billion. Of this $1.192 billion will go to SCE&G for its 55% ownership of the project, with $976 million to Santee Cooper, which owns 45%. Analysis of detailed schedule and cost data provided by Westinghouse and EPC subcontractor Fluor showed unit 2 would not be completed until December 2022 and unit 3 not before March 2024 – four years after the most recent completion date provided by Westinghouse. The overall project was 64.1% complete at the end of March 2017, and "about two-thirds" complete in July.

At the end of July Santee Cooper decided to halt construction in the light of “significant challenges” in completing the two reactors, notably uncertain costs, the uncertain availability of production tax credits, and reduced demand forecast. Also "the current political landscape has reduced the urgency for emissions-free base-load generation." It found that completing the project would cost the company $8 billion plus about $3.4 billion in interest, with schedule delays contributing to the increased interest. It had already spent $4.7 billion on construction and interest to date for its 45% share of the project. SCE&G had been evaluating options, including completion of only one unit, but concluded that completion of both units would be “prohibitively expensive” – about $9.9 billion for its 55% share of the project. SCANA said that completing only unit 2 would have resulted in a combined cost that was less than that previously approved by the South Carolina Public Services Commission under the fixed price option for completing the two nuclear units, but Santee Cooper’s decision ruled this out. “Ceasing work on the project was our least desired option, but this is the right thing to do at this time," and would accordingly apply to the state public services commission to permit this and allow it to recover from ratepayers about $4.9 billion it has spent.

Santee Cooper said that during the project wind-down it will continue to investigate the potential for federal support or "additional partners" that might make the project economic, and SCE&G echoed this. The state government then considered trying to sell Santee Cooper or take other action to revive the project, and SCE&G said in mid-August that it would withdraw its petition to the state public services commission, to allow for possible new partners. Duke Energy said it was not interested.

Westinghouse said: "The South Carolina economy is sure to feel the negative impact of losing over 5000 high-paying, long-term jobs, as well as not having available the reliable, clean, safe and affordable energy these units would provide. Also, at a time when other nuclear plants are being retired, the US energy sector is sure to feel the stunting impact of walking away from these two nuclear units."

In September 2017 the state governor released a report written 18 months earlier by Bechtel, highlighting eight significant contractual and management problems that required resolution*. The report detailed numerous recommendations, but suggested that the most important step for the consortium was to create a new "more achievable" project schedule.

Later in September 2017, SCANA and its subsidiaries received a federal subpoena for a broad range of documents related to the Summer plant expansion.

* The report found that some issues were to be expected due to the choice of reactor type – the project was due to be the first AP1000 reactor built in the USA – and the preceding hiatus in nuclear new build activity in the country. However it also highlighted the following eight significant contractual and management problems that required resolution:

- While the consortium's engineering, procurement and construction plans and schedules are integrated, the plans and schedules are not reflective of actual project circumstances.

- The consortium lacks the project management integration needed for a successful project outcome.

- There is a lack of a planned vision, goals and accountability between the owners and the consortium.

- The contract does not appear to be serving the owners or the consortium particularly well.

- The detailed engineering design is not yet completed, which will subsequently affect the performance of procurement and construction.

- The issued design is often not constructible, resulting in a significant number of changes and causing delays.

- The oversight approach taken by the owners does not allow for real-time, appropriate cost and schedule mitigation.

- The relationship between the consortium partners (Westinghouse Electric Company and Chicago Bridge & Iron) is strained, caused to a large extent by commercial issues.

In September 2020 Santee Cooper and Westinghouse finalized the terms of a settlement over ownership of equipment associated with the VC Summer plant. Earlier in May 2019, Santee Cooper had asked a New York bankruptcy court to dismiss Westinghouse’s claim of ownership of the same equipment. The two companies eventually agreed to split the net sales proceeds for major non-installed nuclear equipment. For major installed nuclear equipment, Santee Cooper was to receive 90% and Westinghouse 10%. For other equipment that could be used in other nuclear projects, 67% of the sale proceeds were to go to Santee Cooper and 33% to Westinghouse. Santee Cooper has 100% ownership of the remaining project equipment. Westinghouse was to have responsibility for marketing the nuclear equipment.

However, Brookfield Asset Management has been in talks to acquire and restart the two units at VC Summer. In October 2025 Santee Cooper’s board approved Brookfield’s proposal, granting the two parties an exclusive negotiation window expected to last several weeks as they finalize terms. In December 2025 the parties signed a memorandum of understanding (MoU) under which Santee Cooper would receive $2.7 billion if a final investment decision is reached. The MoU set a deadline of June 2026 for Brookfield to determine initial feasibility. In May 2026, a joint venture of Brookfield and The Nuclear Company was announced with the goal of completing the units.

The licences under which construction took place were terminated in March 2019 and cannot be re-issued or revived. To continue construction would require new licenses from NRC.

Bellefonte

Tennessee Valley Authority had a pair of uncompleted 1213 MWe PWR reactors: Bellefonte 1&2. Construction on these units was abandoned in 1988 after $2.5 billion had been spent and unit 1 largely (88%) completed and unit 2 about 58% completed. In February 2009, the NRC reinstated the construction permits for these (and later the status of the reactors classified as 'deferred'). Today unit 1 is considered no more than 55% complete due to the transfer or sale of many components and the need to upgrade or replace others, such as the instrumentation and control systems, reactor pressure vessel, steam generators and main condenser tubing. In August 2011 TVA opted to complete unit 1 at a cost of about $4.9 billion rather than building a new AP1000 reactor as unit 3* (see Appendix 3: COL Applications). TVA then asked the NRC in 2011 to defer consideration of its COL for units 3&4 (AP1000 option), and in February 2016 it withdrew the COL application.

* In August 2010, TVA had committed to spending $248 million in the year to September 2011 towards work at Bellefonte8 and an engineering contract was awarded to Areva SA in October 2010 for work on unit 1, including engineering, licensing and procurement of long-lead materials in support of a possible start-up date in the 2018-19 timeframe. Following TVA's 2011 decision to proceed, the Areva contract included construction and component replacement work on the plant's nuclear systems, a digital instrumentation and control (I&C) system, a modernized control room, a plant simulator for personnel training plus fuel design and fabrication. Areva contracts amounted to some $1 billion, with heavy construction to start when Watts Bar 2 was completed. In late 2013 TVA revised the estimated cost to $7.4 to $8.7 billion.

However, TVA’s 20-year integrated resource plan in 2015 did not have Bellefonte 1&2 as a firm prospect, and it projected 2028 completion of unit 1 as having the effect of increasing system costs. Later in 2015 the company said it would defer consideration of completing unit 1 for a decade. In May 2016 the TVA board decided to offer the plant for sale at auction, and in November Nuclear Development LLC agreed to buy it for $111 million.

Nuclear Development said it intended to invest up to $13 billion from 2017 to complete the plant, and it was lobbying for a $5 billion loan guarantee. Bellefonte is a regulated plant, with guaranteed cost recovery. In mid-2018 the company signed an agreement with SNC-Lavalin to finish building the plant once the purchase is completed. Completion of unit 1 was then anticipated in 2024. In November 2018 Nuclear Development applied to the NRC to transfer the construction permits and announced its intention to involve Framatome in the project, but late in 2019 the NRC had not yet undertaken a review of the application. The sale is contingent upon NRC approval, and the company said that construction depends both on a loan guarantee (it was seeking $8.6 billion) and securing power purchase agreements.

Lee

Duke Energy lodged a COL application in December 2007 for two Westinghouse AP1000 units for its William States Lee III plant at a new site near Charlotte in Cherokee County, South Carolina, to provide power for North Carolina. The company was seeking a loan guarantee and was considering regional partnerships to build the plant. The environmental review for NRC was completed in December 2013, showing no problems, the safety evaluation review was completed in August 2016 and the COLs issued in December 2016. Duke told NRC in 2012 that it was revising its COL application to move the nuclear island of both Lee units by some 20 metres to make excavation and construction easier. Duke had spent $471 million on licensing, planning and pre-construction activities for the plant to February 2016. If proceeding, the 1117 MWe (net) units were then expected online in 2024 and 2026. In August 2017 the company announced: "The risks and uncertainties to initiating construction on the Lee nuclear project have become too great, and cancellation of the project is the best option for customers."

In October 2025 Duke Energy filed its 2025 Carolinas Resource Plan, which includes the possibility of deploying large LWR capacity at the Lee site.

Turkey Point 6&7

NextEra Energy subsidiary Florida Power & Light (FPL) applied in June 2009 for a COL for two Westinghouse AP1000 reactors at Turkey Point in Florida where two 693 MWe PWR units (3&4) are operating and were uprated in 2012-13. (Unit 5 is a 1190 MWe combined cycle gas plant; units 1&2 are 400 MWe oil/gas units.) In 2011 the Florida Public Service Commission approved a levy towards construction of the reactors, and in May 2014 the state government approved the project, with new transmission lines.

The company said in April 2014 that it expected to start operation of the first new unit in June 2022 and the second a year later, but in January 2015 changed this to 2027 and 2028, due to “NRC licensing schedule adjustments and changes to the Florida nuclear cost recovery law,“ which delay the start of site works. The COL was approved by the NRC in April 2018.

South Texas Project 3&4

Units 3&4 at South Texas Project (STP) were envisaged as a merchant plant with two 1356 MWe Advanced Boiling Water Reactors (ABWR)j. The COL application was submitted in September 2007 by site operator STP Nuclear Operating Company (STPNOC) on behalf of the project owner, which was then a 50:50 partnership between NRG Energy and the City Public Service Board (CPS Energy) of San Antonio. Ownership of STP units 1&2 (Westinghouse PWRs) is Constellation Energy (44%) – which purchased NRG Energy’s share in November 2023 – CPS Energy (40%) and Austin Energy (16%).

In March 2008, NRG with Toshiba subsidiary Toshiba America Nuclear Energy (TANE) formed Nuclear Innovation North America (NINA – 88% NRG; 12% TANE) to develop the project. In February 2009, TANE entered into an engineering, procurement and construction (EPC) agreement that would convert into a turnkey contract once the final decision to proceed with the project had been taken. Following TANE's later announcement that the project would cost $4 billion more than the $13 billion that was previously estimated, in February 2010 CPS Energy decided to reduce its stake to 7.625%, with NINA increasing its share to 92.375%.

In May 2010, Japanese utility Tokyo Electric Power Company (Tepco), which had been acting as technical consultant to the project, agreed to take 10% of NINA's stake for $155 million, with an option to later double its holding. The deal was conditional on a DOE loan guarantee being awarded to the project. However, in April 2011, based largely on low natural gas prices in Texas compounded by the March 2011 accident at Tepco's Fukushima Daiichi plant in Japan, NRG decided to pull out of the project and write off its $331 million investment in it. Toshiba had spent $150 million and persevered with the project, though it wrote off $305 million (JPY 31 billion) on NINA in 2014. NINA was dissolved in 2018.

COLs for each of the two units were issued in February 2016.k However, Toshiba’s withdrawal of the application for design certification renewal in mid-2016 effectively put the project on hold. In May 2018, Toshiba announced its withdrawal from the project, stating that it was no longer financially viable. Toshiba said its decision to exit the project was in line with its policy "to eliminate risk from the overseas nuclear power business, particularly from construction-related cost overruns in nuclear power plant construction projects." Toshiba stated it had sought, but failed to find investors to participate in the project.

The UAMPS Carbon Free Power Project, a six-module NuScale SMR plant at the Idaho National Laboratory, would be owned by Utah Associated Municipal Power Systems (UAMPS) that comprises 48 members from Utah, California, Idaho, Nevada, New Mexico and Wyoming. UAMPS planned to submit a COL application by January 2024. In 2013 NuScale secured up to $226 million DOE support for the original 45 MWe design. The DOE granted permission to site the plant on the 2300 square km Idaho National Laboratory estate, reportedly in the southern part of it. Under this agreement UAMPS had ten years to begin operating the first module, and this would trigger a 99-year lease for the plant.

In October 2020 the DOE approved a $1.335 billion cost-share award, allocated over 10 years, to a special purpose entity wholly-owned by UAMPS – the Carbon Free Power Project – for the development and construction of the planned six-module plant (then 60 MWe per module). The award represented around one-quarter of the development and construction costs over ten years. Projected LCOE was about $55/MWh. In November 2020, the module power was uprated to 77 MWe, lowering the overnight capital cost from $3600/kWe to $2850/kWe, according to NuScale.

However, a UAMPS meeting held in October 2022 indicated significantly higher costs for the project than first estimated. Inflationary pressures, such as the rising price of steel could push the power cost from $55/MWh to between $90 and $100 per MWh.

In November 2023 UAMPS announced that it had mutually agreed to cancel the CFPP due to the inability to reach the 80% subscription rate required to support the development.

Fermi 3

This is a reference unit for GE Hitachi's ESBWR design, proposed by Detroit Edison in Michigan, but the company has not yet committed to proceeding. A COL application was made in 2008 and environmental approval was received in January 2013. Full design certification of the ESBWR in 2014 allowed the safety evaluation to proceed, and the COL was approved in May 2015.

Levy County, Florida

Site works started for two 1200 MWe Westinghouse AP1000 reactors on a greenfield site in Florida, and to January 2012 some $860 million had been spent on this. The company expected to have spent about $1 billion on the design, acquisition of heavy equipment and site works by the time it secures NRC approval. In September 2008, Progress Energy Florida signed an EPC contract with Westinghouse and The Shaw Group (now CB&I) consortium. The contract is for $7.65 billion ($3462/kWe), of an overall project cost of about $14 billion.

In August 2013 Duke Energy resolved to terminate the 2008 EPC contract as "a result of delays by the NRC in issuing COLs for new nuclear plants, as well as increased uncertainty in cost recovery caused by recent legislative changes in Florida.” It continued to pursue the COLs in order to keep the option open. In April 2014 Duke announced plans to build 2745 MWe of gas-fired capacity by 2021 instead of proceeding with the Levy County nuclear plant in the original timeframe. Duke Energy Florida was planning to sell all the long-lead time equipment it had ordered by the end of 2014, but it was in dispute with Westinghouse over EPC contract termination. In October the Florida Public Service Commission ordered Duke to repay to ratepayers $54 million it had collected in advance to fund the 'cancelled' project. In October 2016 the NRC approved the COLs.

The last estimated operational dates were 2024-25, the delay being due to "lower-than-projected customer demand, the lingering economic slowdown, uncertainty regarding potential carbon regulation and current low natural gas prices." The revised cost was $19-24 billion. It would be a regulated plant, with guaranteed cost recovery. In August 2017 Duke Energy cancelled the project, citing the Westinghouse bankruptcy and slowing energy demand, and said it would not maintain the licences.

North Anna 3