Nuclear Power in Russia

- Russia is moving steadily forward with plans for an expanded role of nuclear energy, including development of new reactor technology.

- It is committed to closing the fuel cycle, and sees fast reactors as key to this.

- Exports of nuclear goods and services are a major Russian policy and economic objective. Russia is currently involved in the construction of about 20 reactors abroad.

- Russia is a world leader in fast neutron reactor technology and is consolidating this through its Proryv ('Breakthrough') project.

Reactors

Construction

Shutdown

Operable nuclear power capacity

Electricity sector

Total generation (in 2023): 1162 TWh

Generation mix: natural gas 511 TWh (44%); nuclear 217 TWh (19%); coal 211 TWh (18%); hydro 202 TWh (17%); oil 9.3 TWh (1%); wind 4.8 TWh; biofuels & waste 3.9 TWh; solar 2.7 TWh.

Import/export balance: 16.53 TWh net export (1.6 TWh imports; 18.1 TWh exports)

Total consumption: 837 TWh

Per capita consumption: c. 5800 kWh in 2023

Source: International Energy Agency. Data for year 2023.

Russia is one of the few countries without a populist energy policy favouring wind and solar generation; the priority is unashamedly nuclear.

Industry development

Russia's first nuclear power plant, and the first in the world to produce electricity in 1954, was the 5 MWe Obninsk reactor. Russia's first two commercial-scale nuclear power plants started up in 1963-64, then in 1971-73 the first of today's production models were commissioned. By the mid-1980s Russia had 25 power reactors in operation, but the nuclear industry was beset by problems. The Chernobyl accident led to a resolution of these, as outlined in the Appendix of the information page on Russia's Nuclear Fuel Cycle.

Between the 1986 Chernobyl accident and the mid-1990s, only one nuclear power station was commissioned in Russia, the four-unit Balakovo, with unit 3 being added to Smolensk. Economic reforms following the collapse of the Soviet Union meant an acute shortage of funds for nuclear developments, and a number of projects were stalled. But by the late 1990s exports of reactors to Iran, China and India were negotiated and Russia's stalled domestic construction programme was revived as far as funds allowed.

Around 2000, nuclear construction revived and Rostov 1 (also known as Volgodonsk 1), the first of the delayed units, started up in 2001, joining 21 GWe already on the grid. It was followed by Kalinin 3 in 2004, Rostov 2 in 2010 and Kalinin 4 in 2011.

By 2006 the government's resolve to develop nuclear power had firmed and there were projections of adding 2-3 GWe per year to 2030 in Russia as well as exporting plants to meet world demand for some 300 GWe of new nuclear capacity in that timeframe. Early in 2016 Rosatom said that Russia’s GDP gained three roubles for every one rouble invested in building nuclear power plants domestically, as well as enhanced “socio-economic development of the country as a whole.”

In 2017 the CEO of Rosatom said that the government would end state support for the construction of new nuclear units in 2020, and so Rosatom must learn to earn money on its own, primarily via commercial nuclear energy projects in the international market. He said that Rosatom had come from being a consortium of unprofitable, separately-run businesses a decade ago to a vertically-integrated state corporation with improved strategies and financial performance, thanks in part to a "large-scale" programme of state funding. “In this situation … we must learn how to earn money independently,” especially in the world market. “Optimisation of the management system should become the main theme of 2017.”

Rosatom's long-term strategy up to 2050 involves moving to inherently safe nuclear plants using fast reactors with a closed fuel cycle, especially under the Proryv ('Breakthrough') project. It envisages nuclear providing 45-50% of electricity at that time, with the share rising to 70-80% by the end of the century. The ultimate aim of the closed fuel cycle is to eliminate the production of radioactive waste from power generation.

Apart from adding capacity, utilization of existing plants has improved markedly since 2000. In the 1990s capacity factors averaged around 60%, but they have steadily improved since and are now above 80%.

See also subsections: Transition to Fast Reactors, and Fast reactors in the Reactor Technology section below.

Nuclear power plants

Russia has 34 operable reactors. Rosenergoatom is the only Russian utility operating nuclear power plants. Its nuclear plants have the status of branches. It was established in 1992 and was reconstituted as a utility in 2001, as a division of Rosatom.

Operable reactors in Russia

Source: International Atomic Energy Agency and World Nuclear Association

V-320 is the base model of what is generically VVER-1000; V-230 and V-213 are generically VVER-440; V-179 & V-187 are prototypes. Rostov was formerly sometimes known as Volgodonsk. Many reactors have been uprated but current net capacities are mostly unknown.

* Novovoronezh II-1&2 are sometimes referred to as Novovoronezh 6&7.

Lifetime extension, uprates and completing construction

Most reactors are being licensed for operating lifetime extension. Over half of Russia's nuclear generation in 2023 came from units which had been upgraded for long-term operation and were operating beyond their initial design lifetimes (around 30 years).

Generally, Russian reactors were originally licensed for 30 years from first power. Since 2000, licence extensions have been issued for: Beloyarsk 3, Novovoronezh 3-5, Kola 1-4, Kalinin 1&2, Balakovo 1-4, Rostov 1, Kursk 1-4, Leningrad 1-4, Smolensk 1-3, and Bilibino 1-4. Novovoronezh 4&5, Kola 1&2, Rostov 1, Bilibino 2-4, and Leningrad 3&4 have been granted second licence extensions.

Generally the VVER-440 units have got 15-year operating lifetime extensions. (Kola 1&2 VVER-440 units are V-230 models which the EU has paid to shut down early in countries outside Russia. Novovoronezh 4, a V-179, is a predecessor to these.) The reactor pressure vessels of some older reactors have undergone thermal annealing to reduce acquired brittleness. Kola 1&2 were upgraded for operating lifetime extension to 60 years – 2033 & 2034. Kola 3&4 licence extensions to 2027 and 2029 (45 years) have been confirmed after upgrading work. Novovoronezh 4 is now licensed to operate until 2032, and unit 5 to 2035.

Most VVER-1000 units are expected to have 30-year operating licence extensions. In 2015 Balakovo 1 was upgraded to extend its operating lifetime to 60 years, followed by the same for unit 2 in 2017, and unit 3 in 2019. Unit 1 was the first large VVER reactor to undergo thermal annealing of the pressure vessel.

RBMK reactors have been uprated and granted 15-year lifetime extensions. Following significant design modifications made after the Chernobyl accident, as well as extensive refurbishment including replacement of fuel channels, 45-year lifetimes have been achieved. In 2023 RBMK units provided just less than one quarter of Russia's nuclear-generated electricity.

For older RBMK units, service lifetime performance recovery (LPR) operations involve correcting deformation of the graphite stack. After dismantling the pressure tubes, longitudinal cutting of a limited number of graphite columns returns the graphite stack geometry to a condition that meets the initial design requirements. The procedure gives each of these older reactors at least three years' extra operation, and may then be repeated. Leningrad 1 was the first reactor to undergo this over 2012-13, followed by the Kursk units, and then Smolensk.

Most reactors have been uprated. In May 2015 Rosenergoatom said it had completed uprating all VVER-1000 reactors to 104% of rated power, and was starting to take them to 107% using advanced TVS-2M fuel design, starting with Balakovo 4. Earlier, uprating of 5% for VVER-440 (but 7% for Kola 4) had been achieved, and in 2015, Kola 3 went to 107%. The overall cost was less than RUR 3 billion ($60.5 million), according to Rosenergoatom. The cost of this was earlier put at US$ 200 per kilowatt, compared with $2400/kW for construction of Rostov 2. Rosatom said that at the end of 2016 all 11 VVER-1000 units then operating were at 104% of their original capacity with Rostechnadzor approval.

Rosenergoatom has been investigating further uprates of VVER-1000 units to 107-110% of original capacity, using Balakovo 4 as a pilot plant to 2014. For the V-320 units, pilot commercial operation at 104% power is carried out over three fuel campaigns, with the reactor and other system parameters being monitored and relevant data collected. After this period, a cumulative 104% power operation report is produced for each plant. Rostechnadzor then assesses safety to license commercial operation at the higher power level.

Rosenergoatom is considering the introduction of a 24-month fuel cycle at new nuclear power units. Previously, VVER-1000 reactors operated for 12 months without refuelling and from 2008 they were all converted to an 18-month fuel cycle. VVER-440s still use a 12-month cycle. To achieve 24 months in new units, the design of VVERs will need to be changed and fuel enrichment would need to be increased from 4-4.5% U-235 to 6-7% in the VVER-TOI design.

Individual operating power plants

Balakovo: Rostechnadzor approved a 4% increase in power from all four Balakovo V-320 reactors and major overhauls were undertaken from 2012. Balakovo 1 was upgraded at a cost of RUR 9 billion over nine years, and in December 2015 Rostechnadzor gave it a 30-year operating lifetime extension, the first Russian unit to achieve this. Rosatom has done the same for the other three units, all of which are uprated to 104% with 18-month refuel cycle. All four Balakovo units have now received 30-year lifetime extensions.

Three test assemblies of REMIX fuel were loaded into Balakovo 3 in June 2016. In September 2021 TVEL announced that the trial of the REMIX fuel over five years had been successful. The first six full assemblies of REMIX fuel were loaded into Balakovo 1 in December 2021 for a five-year trial.

Beloyarsk: Beloyarsk 3 BN-600 fast neutron reactor in Zarechny municipality of Sverdlovsk region was upgraded for a 15-year operating lifetime extension, to 2025, and is now licensed to 2040. In 30 years of operation to late 2011, it produced 114 TWh with capacity factor of 76%. Due to progressive modification, its fuel burn-up has increased from 7% (design value) to 11.4%. It provides heat for Zarechny town as well as electricity from three 200 MWe turbine generators.

The Beloyarsk 4 BN-800 fast neutron reactor was delayed by lack of funds following construction start in 2006 and after first criticality in June 2014 it came online with grid connection in December 2015. Its three steam generators drive a single turbine generator. It entered commercial operation at the end of October 2016. Total cost of construction was reported as RUR 145.6 billion. Despite being a test bed for new fuels, it produced 13.7 TWh in its first 36 months.

Beloyarsk 5 is planned as a BN-1200 reactor (see below).

(Further details on Beloyarsk 4&5 is in the Transition to Fast Reactors and Reactor Technology subsections below.)

Bilibino: Unit 1 was shut down in 2018; units 2-4 were to be shut down in December 2021 after the floating nuclear power plant at Pevek was online, but in 2019 unit 2 was given a licence extension to 2025. Units 2&3 were also granted life extensions to 2025 in September 2023. Decommissioning of unit 1 commenced in January 2019. Units 2-4 were shut down in December 2025. The units were EGP-6 light water graphite-moderated reactors.

Kalinin: Unit 1 had a major overhaul in 2012 for licence extension and power uprate, and Kalinin 2 followed to 2016. Unit 3 was officially approved for this in June 2019. Kalinin 1 was undergoing tests at 104% in 2013 and in mid-2014 it was granted a ten-year licence extension, to mid-2025. In July 2025 its licence was extended by a further 19 years to June 2044. Kalinin 2 licence extension to 2038 was granted in November 2017. All four Kalinin units are set for a 60-year operating lifetime.

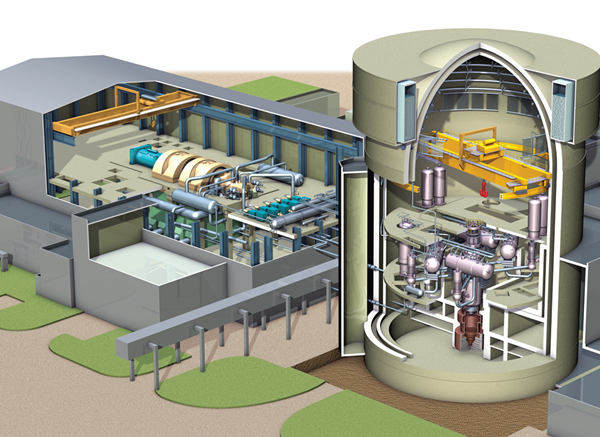

Kalinin 4 is a V-320 unit built by Nizhny-Novgorod Atomenergopoekt. Rostechnadzor approved an operating licence in October 2011, it started up in November, was grid-connected in December and attained full commercial operation in September 2012. It uses major components originally supplied for Belene in Bulgaria. Final cost was RUR 7 billion ($220 million) under budget – about 10%. Silmash (Power Machines) upgraded the turbine generator of units 3&4 to increase their gross power to 1100 MWe in 2016.

Preparing Kalinin 4 for startup (Rosatom)

Kola: Kola 3&4 have received licence extensions to 2027 and 2029 respectively. Both units have been uprated to 107%. Low power demand in the Murmansk region and Karelia means they are not fully utilized.

Kola 1&2 have each received second 15-year licence extensions to 2033 and 2034.

Annealing of the unit 2 reactor vessel was undertaken in 2016, with the service life extended to the end of 2029. Work to extend the operating period of unit 1 to 60 years started in 2016, and in July 2018 it was granted a licence extension to 2033. It was reconnected to the grid in December 2018 after a 250-day shutdown, including annealing of the reactor vessel. Further work was undertaken on unit 2 in 2019 during a 268-day outage, including the introduction of new active and passive safety systems, enhancement of the seismic stability of reactor equipment, and replacement of radiation monitoring, control, reactor protection and diagnostic systems. In December 2019 it was granted a licence extension to 2034. Previous annealing of units 1&2 had been undertaken in 1989, followed by further major works over 1991 to 2005, costing $718 million. Some $96 million of this was from international sources including neighbouring countries.

The Kola reactors will be the first VVERs to run on reprocessed uranium (RepU) as a matter of course.

Kursk: Having had a licence extension to 2016, Kursk 1 was the first RBMK unit to be licensed for pilot operation with 5% uprate (reported to 1020 MWe net) but units 2&4 were also operating at this level late in 2011. In February 2012 Rosatom said it would invest a further RUR 30 billion in upgrading Kursk 2-4 and extending their operating lives – RUR 5.0, 11.9 & 13.7 billion respectively.

On units 1&2 work on the graphite moderator stack was undertaken to avoid the deformation experienced in Leningrad 1. Unit 2 was returned to service in February 2014 after its ‘lifetime performance restoration program’. Following inspection, further work was postponed for unit 1, and was then completed in April 2016. Kursk 4 was issued a 15-year licence extension to December 2030 after RUR 13 billion in upgrade work over ten years. Kursk 1 was shut down in December 2021, and Kursk 2 was shut down in January 2024 – both after 45 years in operation.

Units 3-4 are each set for 45-year operating lifetimes.

Kursk 5 – an upgraded RBMK design – was more than 70% built before the project was terminated. Rosatom was keen to see it completed and in January 2007 the Duma's energy committee recommended that the government fund its completion by 2010. However, funds were not forthcoming and the economic case for completion was doubtful, so in February 2012 Rosatom abandoned the project. Instead, major announcements were made regarding Kursk II (see below).

Leningrad: In 2010, intended life extension was announced for Leningrad 4 (15 years), and it underwent a RUR 17 billion refurbishment over 2008-11, including replacement of generator stator. The upgrading investment in all four Leningrad RBMK units totalled RUR 48 billion to early 2012. Leningrad unit 1 was shut down in May 2012 due to deformation of the graphite moderator, and after a RUR 5 billion restoration of the graphite stack as the pioneer lifetime performance recovery (LPR) procedure it was restarted in November 2013. The same work was undertaken on unit 2 in 2014.

Unit 1 was finally shut down in December 2018, followed by unit 2 in November 2020. Defuelling of unit 2 was completed in December 2024. Units 3&4 have been granted licence extensions to 2030. Two VVER-1200 units of phase II of the project are in operation, and a third is under construction. One further unit is planned at the site.

Novovoronezh: Units 3&4 gained 15-year licence extensions to 2016 and 2017, then unit 4 was given a further 15-year licence extension, using parts from the shutdown unit 3. They were the first VVER-440 units to have their operational life extended by annealing the reactor pressure vessels. In 2018 the emergency core cooling system of unit 4 was supplemented so that a drop in primary circuit pressure will automatically release water with boric acid into the core.

A plan for refurbishment, upgrade and life extension of Novovoronezh 5 was announced in mid-2009, this being a prototype of the second-generation VVER-1000 design. The initial estimate was RUR 1.66 billion but this eventually became RUR 14 billion. The 12 months of work from September 2010 included the total replacement of the reactor control system and 80% of electrical equipment, and fitting upgraded safety systems, in particular, those of emergency core cooling and feedwater, and emergency power supply. The unit is now licensed to 2035.

Unit 6 (also referred to as Novovoronezh II-1), the first of a new generation of 1200 MWe class reactors, was grid-connected in August 2016 after about eight years' construction, and unit 7 (unit II-2) was grid-connected in April 2019.

Rostov: In September 2009 Rostechnadzor approved an operating licence for Rostov 2; it started up in January 2010, was grid connected in March, and entered commercial operation in October 2010. It was approved for 104% of nominal power in October 2012, to about 1075 MWe gross. Accident tolerant fuel (ATF) has been in testing in Rostov 2 since 2021. In September 2024 the third 18-month cycle of ATF began.

Rostov 3&4 are effectively new V-320 units. Unit 3 construction restarted in September 2009. It started up and was grid connected in December 2014, reached full power in July 2015, and entered commercial operation in September 2015. In December Rostechnadzor approved a power increase to 104% of the rated level. Unit 4 construction started in June 2010. It started up late in 2017, was grid connected in February 2018 and entered commercial operation in September 2018. See also following section.

Smolensk: Early in 2012 Rosatom announced a RUR 45 billion programme to upgrade and extend the operating lifetime of Smolensk 1-3 RBMK units. At the same time, construction of Smolensk II was to get underway, with the first VVER unit then to come online by 2024 (now expected 2033). In 2012 Smolensk 1 was licensed to December 2022, a ten-year extension after refurbishment. It has since been licensed to 2027. Upgrading unit 2 was undertaken from 2013, and included replacement of fuel channels and upgrading the reactor control and protection system and radiation monitoring system, as well as reinforcing the building structure. It is licensed to operate until May 2030. Unit 3 upgrade was implemented to March 2019, though it was already operating above 1000 MWe gross. It is licensed to 2034.

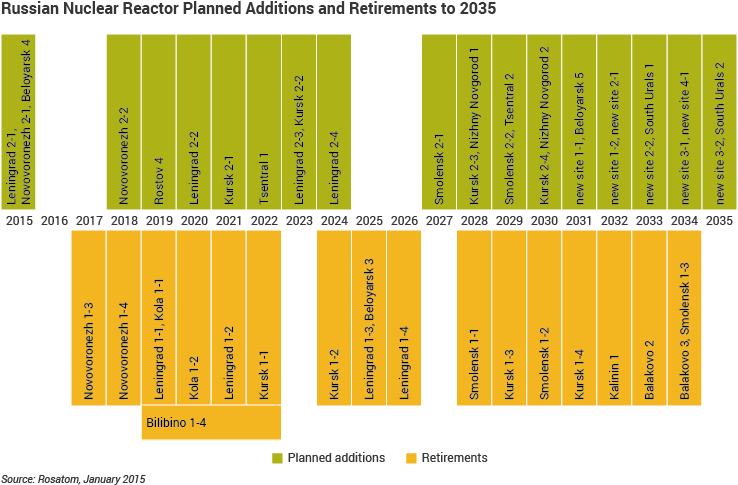

New nuclear capacity

There are six reactors currently under construction in Russia.

Under construction reactors in Russia

In June 2022 Strana Rosatom said that the government has set a goal to bring the share of nuclear power in electricity supply to 25%. Rosenergoatom said that would be challenging because some 10 units are due to shut down by 2030. In order to offset these retirements, Rosenergoatom has said it would need to increase efficiency at operating units. Among other measures, it aims to transfer all VVER-1200 power units to an 18-month fuel cycle.

A draft plan released in September 2024 by the Unified Energy System (UES) of Russia proposed that by 2042 the share of electricity generated by nuclear power will have increased to 23.5%. The draft plan includes 34 new nuclear power units, which are listed in the tables of planned and proposed reactors below. In April 2025 the government approved the Energy Strategy of the Russian Federation until 2050, which targets a 25% nuclear share by 2045 and instructs the construction of 38 new nuclear power units.

Earlier plans are detailed in the appendix.

Russia's long-term goal is to move to fast neutron reactors and closed fuel cycle, outlined below in the Transition to Fast Reactors section.

Power reactors planned

| Reactor | Reactor type | MWe gross | Deployment |

|---|---|---|---|

| Beloyarsk 5 | BN-1200 | 1220 | 2035 |

| Khabarovsk 1&2 | VVER-600/V-498 | 2 x 600 | 2036 |

| Kola II 1-4 | VVER-600/V-498 | 4 x 600 | 2035 |

| Krasnoyarsk 1-4 | VVER-1200/V-510 | 4 x 1255 | 2037 |

| Kursk II-4 | VVER-TOI | 1255 | 2032 |

| Novocherkassk 1&2 | VVER-1200/V-510 | 2 x 1200 | 2036 |

| Primorsk 1&2 | VVER-600/V-498 | 2 x 600 | 2039 |

| Reftinskaya 1 | VVER-1200/V-510 | 1255 | 2036 |

| Smolensk II 1&2 | VVER-1200/V-510 | 2 x 1250 | 2033 |

| South Urals 1&2 | BN-1200 | 2 x 1220 | 2038 |

| Ust-Kuyga, Yakutia 1&2 | RITM-200N | 2 x 55 | 2030 |

| Total of 23 planned | 22,200 GWe |

VVER-1200/V-510 is the reactor portion of the VVER-TOI plant. South Urals was to be BN-800, and now is to be BN-1200.

South Ural is at Ozersk, Chelyabinsk region, 140 km west of Chelyabinsk in Sverdlovsk region. Primorsk is in the far east.

Power reactors proposed

| Reactor | Reactor type | MWe gross |

|---|---|---|

| Cape Nagloynyn, Chukotka | Shelf-M | 10 |

| MPEB Baimsky Chukchi 1-4 | RITM-200S | 4 x 106 |

| Norilsk ASMM 1-4 | RITM-400 | 4 x 80 |

Rostov 2, 3&4 (formerly Volgodonsk)

The environmental statement and construction application were approved by Rostechnadzor in May 2009, the construction licence was granted to Energoatom in June, and construction resumed about September (it had started in 1983). First new concrete for unit 4 was in June 2010. The plant is 13.5 km from the city on the banks of Volgodonsk Tsimlyansk reservoir. Rosatom brought forward the completion dates of the two units after deciding that they would have V-320 type of VVER with improved steam generators and capacity of 1100 MWe. This was expected to save some RUR 10 billion relative to the AES-2006 technology, as it continued the construction done over 1983-86.

OMZ's Izhorskiye Zavody facility at Izhora provided the pressure vessel for unit 3. Nizhniy Novgorod Atomenergoproekt (now NIAEP-ASE) was principal contractor for units 3&4, expected to cost 130 billion according to Rosenergoatom in August 2012. Steam generators for unit 4 were from AEM-Tekhnologi at the Atommash plant, those for unit 3 from ZiO-Podolsk. Ukraine's Turboatom provided the low-speed turbine generators for both units. Grid connection of unit 2 was in March 2010 and full commercial operation was in October. Unit 3 started up and was grid-connected in December 2014, and entered commercial operation in September 2015. Unit 4 started up in December 2017, was grid-connected five weeks later in February 2018 and entered commercial operation in September 2018. The Rostov power plant supplies Crimea, annexed by Russia in 2014.

Novovoronezh II

The principal contractor for Novovoronezh Phase II is JSC AtomEnergoProekt (Moscow), with work starting in 2007 and some involvement of NIAEP-ASE. Construction is now under the ASE group. This was the lead plant for deploying the V-392M version of the AES-2006 units. First concrete was poured for unit 1 (the 6th unit at the site) in June 2008 and for unit 2 in July 2009. Unit 1 was initially expected to be commissioned in 2015, with unit 2 following a year later, at a total cost of US$ 5 billion for 2228 MWe net (1114 MWe net each). The reactor pressure vessels are from OMZ Izhora and the advanced steam generators from ZiO-Podolsk, with 60-year operating lifetime expectancy. Turbine generators (high speed) are from Power Machines.

Atomenergoproekt told its contractors in December 2014 to accelerate work, but in May 2015 a delay of one year in commissioning both units was announced, due to low power demand. In September 2015 a pre-startup peer review was conducted for unit 1 under World Association of Nuclear Operators (WANO) auspices. Rostechnadzor issued the operating licence for unit 1 in March 2016, and fuel loading commenced. It started up in May and was grid-connected in August 2016. Unit 2 was due to enter commercial operation in January 2019, but in February 2018 Rosenergoatom announced that it would slow construction in response to slowing demand and pressure from power consumers to reduce rate increases. Fuel loading was completed in February 2019, with grid connection in May, and commercial operation in October 2019. The plant is on one of the main hubs of the Russian grid.

In July 2020, Rosenergoatom announced that unit 1 would switch to an 18-month refuelling cycle (from 12 months) for a trial period of about three years.

Leningrad II

A general contract for Leningrad phase II AES-2006 plant was signed with St Petersburg Atomenergoproekt (SPb AEP, merged with VNIPIET to become Atomproekt) in August 2007 and Rostechnadzor granted site licences in September 2007 for two units. A specific engineering, procurement and construction contract for the first two V-491 units was signed in March and Rostechnadzor issued a construction licence in June 2008. First concrete was poured on schedule for unit 1 in October 2008 and it was due to be commissioned in October 2013. However, a section of outer containment collapsed in 2011 and set back the schedule, as did subsequent manpower shortage, so that commissioning was then expected in 2016, following start-up at the end of 2015. Rostechnadzor granted a construction licence for the second reactor in July 2009, and first concrete was poured in April 2010. Commercial operation was due in 2018 but in May 2015 a delay of one year in commissioning both units was announced, due to low power demand. Unit 1 achieved first criticality in February 2018, and was grid connected in March, with Rostechnadzor approving commercial operation by October 2018. Rosenergoatom then announced a delay to the start of commercial operation of unit 2 to 2020. The delay was requested by energy consumers to reduce rate increases. In July 2020 Rosatom reported that first fuel assemblies had been loaded, and the reactor was connected to the grid in October 2020. Unit 2 entered commercial operation in March 2021 following a delay due to measures to limit the spread of coronavirus. Each reactor will also provide 1.05 TJ/h (9.17 PJ/yr) of district heating. They are designed to replace the oldest two Leningrad units, which shut down in 2018 and 2020.

The 2008 construction contract was for $5.8 billion ($2480/kW) possibly including some infrastructure. Total project cost was estimated at $6.6 billion. In May 2015 Titan-2 became general contractor for units 1&2*, with Atomproekt remaining the general designer, and in October 2015 Titan-2 became also the principal equipment supplier. Construction is now under the ASE group which consolidates most of the entities involved.

* It was reported in September 2011 that Titan-2, a major subcontractor, took over from SPb AEP as principal construction contractor, then in February 2012 that Spetsstroy of Russia (Federal Agency for Special Construction) would do so. In December 2013 Roesenergoatom transferred the project from Spetsstroy to Atomenergoproekt Moscow as principal contractor, while SPb AEP/VNIPIET/Atomproekt remained architect general. NIAEP-ASE also bid for the general contract in October 2013. Rosatom had said in February 2012 that it did not believe that SPb AEP should perform the full range of design, construction and equipment supply roles.

A design contract for the next two units (3&4) was signed with SPb AEP in September 2008, and public consultation on these was held in Sosnovy Bor in mid-2009. An environmental review by Rostechnadzor was announced for them in January 2010 and site development licences were granted in June, then renewed in April 2013. Rosenergoatom signed a contract with VNIPIET at the end of December 2013 to develop project documentation. It expected construction licences in 2014 and construction start in 2015, but the delay to units 1&2 extended to units 3&4.

Construction of Leningrad II-3 commenced in March 2024, followed by Leningrad II-4 in March 2025.

Nizhny Novgorod

The plant in Navashino District near Monakovo was to comprise four AES-1200 units of 1150 MWe net and cost RUR 269 billion. The first was originally planned to come online by 2019 to address a regional energy deficit. In February 2008 Rosatom appointed Nizhny-Novgorod Atomenergoproekt (NN-AEP or NIAEP) as the principal designer of the plant. Rostechnadzor issued a positive site review for units 1&2 early in 2010 and a site licence with prescription for site monitoring in January 2011. Rosatom's proposal to proceed with construction of two units was approved in November 2011. Site works started in 2012 and formal construction starts were expected soon after. This was to be the first VVER-TOI plant, with rated capacity of 1255 MWe per unit. In the government decree of August 2016 two VVER-TOI were specified, for completion by 2030. However the plant was not included in Russia's draft energy plan, released in September 2024.

Tatar

A 4000 MWe nuclear plant was under construction and due on line from 1992, but construction ceased in 1990. Then a two-unit VVER-1200 plant was included in the Regional Energy Planning Scheme in November 2013. In the government decree of August 2016 a single VVER-TOI was listed for completion by 2030 at Kamskiye Polyany in Nizhnekamsk Region of Tatarstan. Russia's draft energy plan in September 2024 did not list a plant at Tatar.

Central/Kostroma

The 2340 MWe Tsentral (Central) nuclear power plant was to be 5-10 km northwest of Buisk Town in the Kostroma region, on the Kostroma River. It was another of those deferred but following Rosatom's October 2008 decision to proceed, it appeared that construction might start in 2013. Rostechnadzor approved the site and a development licence was expected by mid-2010, then a construction licence in 2012. A two-unit VVER-1200 plant was included in the Regional Energy Planning Scheme in November 2013, with both VVER-TOI units to be online by 2030. Moscow Atomenergoproekt was to be the architect-engineer. However, the plant was not in Russia's draft energy plan released in September 2024.

South Urals

The Yuzhnouralskaya plant near Ozersk in Chelyabinsk region has been twice deferred, and was then reported by local government to have three BN-1200 fast reactor units planned, instead of four VVER-1200. Then a two-unit BN-1200 plant was included in the Regional Energy Planning Scheme in November 2013. Plans for an initial BN-1200 unit were confirmed in August 2016, for completion by 2030. There is only enough cooling water (70 GL/yr) for two of them, and the third will depend on completion of the Suriyamskoye Reservoir. The plant was not included in Russia's draft energy plan, released in September 2024.

Kola II

In January 2012 Rosenergoatom said that the replacement Kola II plant, about 10 km south of the present plant in the Murmansk region and on the shores of Lake Imandra, would be brought forward and built with two VVER-TOI units to come on line in 2020. Then a two-unit VVER-1200 plant was included in the Regional Energy Planning Scheme in November 2013; but in September 2014 Rosenergoatom was considering medium-sized units, either VVER-600 or VBER-600 for Kola. In the government decree of August 2016 a single VVER-600 was specified, for completion by 2030. In June 2021 the plant management announced that construction would start on two VVER-S-600 reactors for Kola II in 2028, with the first to be online in 2034. The ‘S’ signifies spectral shift control, with heavy water in the primary coolant. Russia's draft energy plan, released in September 2024, showed three VVER-600 units starting construction between 2035 and 2040. In 2025 Rosatom confirmed plans for four VVER-S-600 units at Kola II, with construction start in 2028 and the first unit online in 2034.

Kursk II

It was originally envisaged that the first unit of Kursk II should be online by the time Kursk 1 closes, then envisaged in 2016. In March 2011, the State Duma’s Energy Committee recommended that the government update the general scheme of deployment of electricity generators, to have units 1 and 2 of Kursk II being commissioned in 2020 and 2023 as the lead project with VVER-TOI types, and Kursk II-1 being the reference unit for VVER-TOI. Kursk I-5 capacity had been planned in the federal target programme and its abandonment left a likely base-load shortfall for UES in central Russia.

Rosatom started engineering surveys for Kursk II in 2011, and set up a task force of representatives from the nuclear industry and Kursk Region government to produce project documentation on construction of Kursk II. In June 2012 Rosatom appointed Moscow AEP as designer, and Nizhny-Novgorod AEP (NIAEP) as architect general and principal contractor.Site work commenced at the end of 2013, with environmental assessment. In June 2016 Rostechnadzor issued a construction licence to Rosenergoatom for unit 1, and the main site works commenced later that month. A licence for unit 2 was issued in October 2016. Atommash supplied the reactor pressure vessels and steam generators, Power Machines the turbine generators, and Energoteks the core catcher. Construction of Kursk II-1 started in April 2018, and unit 2 in April 2019. Kursk II-1 achieved first criticality in May 2025 and was connected to the grid in December 2025. It reached full power in March 2026, with commercial operation expected later in 2026.

Earlier, in March 2025, Rostechnadzor issued site licences for Kursk II-3&4. First concrete was poured for Kursk II-3 in January 2026.

Smolensk II

Atomenergoproekt Moscow was architect engineer for VVER-TOI units to replace old RBMK capacity at Smolensk. Rosenergoatom’s investment concept was approved in 2011. Site surveys were undertaken from June 2013, and three potential sites were shortlisted. In mid-2017 a special decree was issued for the purchase of 400 ha and for site works 6 km from Smolensk I. A four-unit VVER plant was included in the Regional Energy Planning Scheme in November 2013, with two units on line by 2025 and two by 2030. Engineering surveys were completed in November 2014 at Pyatidvorka (6 km from Smolensk I). Construction start was then deferred to 2022, with the first unit expected online in 2027. Rostechnadzor was expected to issue a site licence in September 2016. Russia's draft energy plan, released in September 2024, shows Smolensk II-1&2 as VVER-TOI units due to start construction in 2033 and 2035 respectively. Site preparation and infrastructure construction began in 2025.

Seversk

The first 1200 MWe unit of the Seversk AES-2006 plant 32 km northwest of Tomsk was due to start up in 2015 with the second in 2017. A two-unit VVER-1200 plant was included in the Regional Energy Planning Scheme in November 2013, but did not proceed. both units to be on line by 2030. The plan was for plant to supply 7.5 PJ/yr of district heating. Seversk is the site of a major enrichment plant and former weapons facilities.

Atomenergopoekt Moscow was to build the plant at estimated cost of RUR 134 billion ($ 4.4 billion). Rostechnadzor granted a site development licence in November 2009 and a further site licence in 2011. Provisional site work had commenced, and a design contract for the low-speed turbine generators had been signed between Moscow AEP which was responsible for design and engineering, and Alstom Atomenergomash.

This would be the first Russian plant using the low-speed turbines.

In 2019 Seversk was put on the updated general scheme of deployment of energy facilities, with the first reactor commissioning before 2020 and the second one 2020-2025. However, in the government decree of August 2016 a single BREST-300 fast reactor was the only unit specified, which began construction in June 2021. Russia's draft energy plan, released in September 2024, did not show any further units planned at Seversk.

Baltic

Separately from the February 2008 plan, Rosatom energy-trading subsidiary InterRAO UES proposed a Baltic or Baltiyskaya AES-2006 nuclear plant in Kaliningrad on the Baltic coast to generate electricity for export, and with up to 49% European equity. Private or foreign equity would be an innovation for Russia. The plant was designed to comprise two 1200 MWe VVER units, V-491 model, sited at Neman, on the Lithuanian border and costing some RUR 194 billion (in 2009 value, €4.6 billion, $6.8 billion), for 2300 MWe net. Project approval was confirmed by government decree in September 2009, following initial approval in mid-2008 as an amendment to the federal target program (FTP) of 2007. The mid-2011 business plan estimated the likely capital cost to be €6.63 to 8.15 billion.

WorleyParsons was appointed technical consultant for the project. Rosenergoatom set up a subsidiary: JSC Baltic NPP to build and commission the plant. St Petersburg Atomenergoproekt - VNIPIET (now merged as Atomproekt) was to be the architect engineer, Nizhniy Novgorod AEP (NIAEP) was to be construction manager, with Atomstroyexport (ASE). TitanStroyMontazh was to be engineering subcontractor. Originally AEM Petrozavodskmash was to produce the pressure vessel for unit 1 but this was assigned to AEM-Tekhnologii at the Atommash plant. OMZ's Ishorskiye Zavody was to produce the pressure vessel for unit 2 and the pressurizers for both units. Alstom-Atomenergomash was to supply the Arabelle low-speed turbine generators for both units – the plant was to be the JV's first customer, and the Baltic plant was to be the first Russian plant to use major foreign components. (LMZ high-speed turbine generators had initially been approved.)

Site work began in February 2010. Expenditure to January 2012 was RUR 7.25 billion ($241 million), and that in 2012 was expected to be RUR 7 billion. Rostechnadzor issued a construction licence for unit 1 in November 2011 and first concrete was poured on (revised) schedule in April 2012, with the base completed in December 2012. Unit 1 was planned to come on line in October 2016, after 55 months construction, supplying Rosenergoatom. Commercial operation was due in 2017. Second unit construction was planned over 2013-18, with 48 months to first power and full operation in April 2018. NIAEP-ASE suspended construction in June 2013 (see below), pending a full review of the project intended to be by mid-2014, though some work on the containment was ongoing in following months. Rosenergoatom said that in October 2013 it had spent RUR 50-60 billion ($1.2 to 1.6 billion) on the project. In 2017 the pressure vessel made for unit 1 was sent to Ostrovets in Belarus, replacing one that had suffered a mishap there.

InterRAO UES was responsible for soliciting investment (by about 2014, well after construction start) and also for electricity sales. The Baltic plant would have directly competed with the unit that was planned at Visaginas near Ignalina in Lithuania and with plans for new nuclear plants in Belarus and Poland. Rosenergoatom said that the plant was deliberately placed "essentially within the EU" and was designed to be integrated with the EU grid. Most of the power (87% in the mid 2011 business plan) was to be exported to Germany, Poland and Baltic states. Transmission to northern Germany was to be via a new undersea cable, and in 2011 Inter RAO and Alpiq agreed to investigate an 800 MWe undersea DC link to Germany's grid. Lithuania was invited to consider the prospect, instead of building Visaginas as a Baltic states plus Poland project, but declined.

* Lithuania’s revised energy policy in 2012 involved rebuilding its grid to be independent of the Russian/Belarus system and to work in with the European Network of Transmission System Operators (ENTSO) synchronous system, as well as strengthening interconnection among the three Baltic states.

Czech power utility CEZ earlier expressed interest in the project, as did Iberdrola from Spain, whose engineering subsidiary already has worked at Kola, Balakovo and Novovoronezh nuclear power plants. In April 2010 Enel signed a wide-ranging agreement with Inter RAO which positioned it to take up to 49% of the plant, but this did not proceed. Rosatom earlier said that the project would not be delayed even if 49% private equity or long-term sales contracts were not forthcoming.

However, in June 2013 construction was suspended due to lack of interest in the project from the Baltic states, Poland and Germany. Construction has remained stalled since then, but some manufacture and supply of equipment continued. The polar crane was delivered in August 2014, and a contract for storing four steam generators for 15 months from July 2015 was let for RUR 46 million.

In July 2015 Kaliningrad local government was talking up the prospects of an aluminium smelter to justify resuming construction of the plant. However, in September 2015 the first deputy director general for operations management at Rosatom said that only when long-term electricity sales contracts are negotiated and “formalized in binding documents, i.e. contracts for buying electricity produced by plant from the western side, we could speak of continuation of construction.”

In April 2017 it was confirmed that the RPV fabricated for Baltic 1 would be sent to Belarus for Ostovets 2. See also grid implications in Electricity Transmission Grids information page.

Other reactor designs have been considered at Kalingrad. NIAEP said in 2013 it was investigating building some small nuclear plants in Kaliningrad instead – eight 40 MWe units such as those on floating nuclear power plants was mentioned as a possibility, and they would fit into the local energy system better, with its 500 MWe total requirement. In mid-2014 Rosenergoatom was considering a VVER-600 from Gidropress with many of the same components as the original VVER-1200, and a VBER-600 from OKBM, the latter being less developed so involving a two-year delay. A new schedule and site configuration, involving small units, was to be approved by mid-2014, but this did not proceed.

The 2015 Rosenergoatom annual report said: “Rosatom State Corporation has recently updated the concept for the Baltic NPP project implementation and is supposing to supply up to 100% of power outside the Kaliningrad Oblast. As part of ensuring the technical capability to supply power, several options for the power generation pattern of the Baltic NPP are being studied, taking into account future configuration of synchronization zones, and the Kaliningrad Oblast plans to prepare for an isolated mode of operation. As part of ensuring commercial conditions of supplies, the negotiations with potential buyers of electricity in the EU countries are continued. So far, several memoranda of understanding, and electricity purchase and sale agreements have been signed with major European energy holdings.”

As well as the Baltic plant, two other ventures with Rusal (see below) were to require private equity, but these did not proceed.

Tver

The plant at Udomlya district and 4 km from Kalinin was being designed by Nizhny-Novgorod Atomenergoproekt (NN-AEP), and in January 2010 it was announced that Rostechnadzor would conduct an environmental review of it for the first two VVER-1200 units, these being on the general scheme of electricity generators deployment to 2020. No firm dates have been given for the project, though a site development licence was expected in March 2010.

Pevek

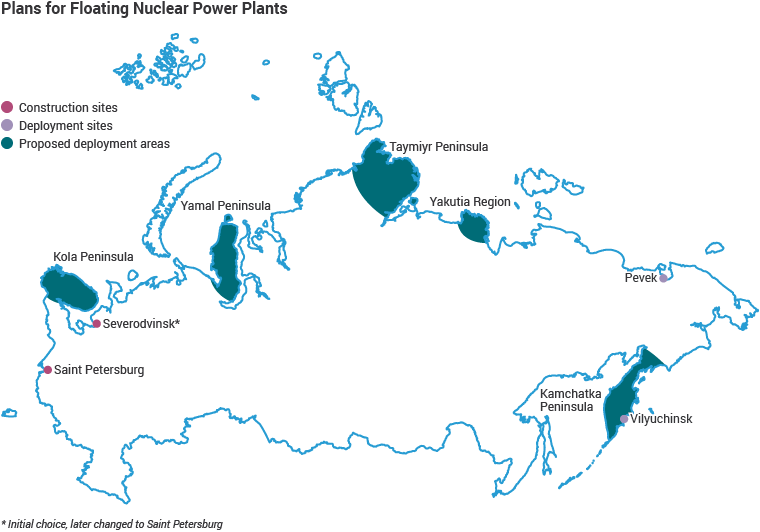

Energoatom signed a RUR 9.98 billion purchase contract for the first floating nuclear power plant then intended for Vilyuchinsk, on the Kamchatka Peninsula in the Far East, in 2009. Keel-laying took place in April 2007 at the Seymash shipyard in Severodvinsk on the White Sea, but the project was then transferred to the Baltiyskiy Zavod shipyard at St Petersburg. A second keel-laying took place in May 2009 at Baltiyskiy Zavod shipyard. The 2x35 MWe plant, named Academician Lomonosov, was due to be commissioned in 2012, but the project was delayed due to shipyard insolvency. In 2012 the plant was re-assigned to Pevek in the far northeast of Siberia. The twin reactors commenced operation in December 2019, with commercial operation in May 2020. See FNPP subsection below.

Transition to fast reactors

It is envisaged that fast neutron power reactors will play an increasing role in Russia, with substantial recycle of fuel.

Russia envisages full recycling of fuel, balancing thermal and fast reactors, so that 100 GWe of total capacity requires only about 100 tonnes of input per year, from enrichment tails, natural uranium and thorium, with minor actinides being burned. About 100 t/yr of fission product waste would go to a geological repository.

The sodium-cooled BN-series fast reactor plans are part of Rosatom's Proryv, or 'Breakthrough', project to develop fast reactors with a closed fuel cycle whose mixed oxide (MOX) fuel will be reprocessed and recycled. The BN-600 reactor at Beloyarsk has operated successfully since 1980 and is now licensed to 2040. The BN-800 reactor at Beloyarsk has operated since 2014, essentially as a demonstration unit for fuel and design features for the BN-1200, which is now deferred.

Recent priority in financing has been for lead-cooled fast neutron reactors with dense nitride fuel. Initially two projects were proposed – the BREST-300 lead-cooled fast reactor with associated nitride fuel fabricating/re-fabricating and spent fuel reprocessing facilities and the SVBR-100 lead-bismuth fast reactor, since dropped. Hence from the mid-2020s, fast reactors will be new designs such as BREST with a single core and no blanket assembly for plutonium production. The first BREST-OD-300 reactor commenced construction in June 2021 at Seversk.

Fast reactors represent a technological advantage for Russia. In late 2012 Rosatom said that it would make available its experimental facilities for use as part of the Generation IV International Forum, including large physical test benches at Obninsk’s Institute of Physics and Power Engineering, the BOR-60 research reactor at NIIAR, and the multifunction research reactor MBIR that is under construction at the NIIAR site.

While Rosatom plans to invest its own funds into FNR development through to 2025, in October 2018 it asked the government to allocate an additional RUR 200 billion ($3.05 billion) over 2019-2025 under the federal target programme for nuclear power. BREST is the focus of this, and Rosatom's long-term strategy up to 2050 involves moving to inherently safe nuclear plants using fast reactors with a closed fuel cycle and MOX or nitride fuel.

Further details of fast neutron power reactors are in the Reactor Technology section below.

Federal Target Programme: Advanced Nuclear Power Technologies 2010-2020

Rosatom put forward two fast reactor implementation options for government decision in relation to the federal target programme (FTP) 'Advanced Nuclear Power Technologies 2010-2020'. The first focused on a lead-cooled fast reactor such as BREST with its fuel cycle, and assumed mobilization of all available resources on this project with a total funding of about RUR 140 billion (about $3.1 billion). The second multi-track option was favoured, since it involved lower risks than the first. It would result in technical designs of the Generation IV reactor and associated closed fuel cycles technologies by 2014, and a technological basis of the future innovative nuclear energy system featuring the Generation IV reactors working in closed fuel cycles by 2020. A detailed design would be developed for a multi-purpose fast neutron research reactor (MBIR) by 2014 also. This second option was designed to attract more funds apart from the federal budget allocation, was favoured by Rosatom, and was accepted.

In January 2010 the government approved the federal target programme (FTP2010) "New-generation nuclear energy technologies for the period 2010-2015 and up to 2020" designed to bring a new technology platform for the nuclear power industry based on fast neutron reactors. It anticipated RUR 110 billion to 2020 out of the federal budget, including RUR 60 billion for fast reactors, and subsequent announcements started to allocate funds among three types: BREST, SVBR (now dropped) and continuing R&D on sodium cooled types.

The FTP involved plans to build and commission a commercial complex to fabricate dense fuel, to complete construction of a pilot demonstration pyrochemical complex to fabricate BN fuel, and to test closed fuel cycle technologies. Fusion studies are included and the total R&D budget was RUR 55.7 billion, mostly from the federal budget. The FTP2010 implementation was intended to result in a 70% growth in exports of high technology equipment, works and services rendered by the Russian nuclear industry by 2020. It was also to commercialize new fast neutron reactors for Russia to build over 2020-2030. In 2012 the head of Rosatom said that the FTP was being accelerated to bring forward development and have a full range of fast reactor technologies with associated fuel cycles operating by 2020. Rosatom's R&D budget would be almost doubled by then to achieve this.

In March 2017 Rosatom and Russian Venture Company (RVC) signed an agreement to cooperate in the promotion of advanced technologies and innovative developments at Rosatom’s subsidiaries. RVC is a Russian state institution responsible for funding national innovation projects on behalf of the National Technology Initiative (NTI), established in 2014. The agreement has wide scope.

Federal target programme 2010 funding for fast neutron reactors to 2020

| Cooling | Demonstration reactor | Construction (RUR billion) | R&D (RUR billion) | Total (RUR billion) |

|---|---|---|---|---|

| Pb-Bi cooled | SVBR 100 MWe | 10.153 | 3.075 | 13.228 |

| Na cooled | (BN-600, BN-800) | 0 | 5.366 | 5.366 |

| Pb cooled | BREST 300 MWe | 15.555 | 10.143 | 25.698 |

| multiple | MBIR 150 MWt | 11.390 | 5.042 | 16.432 |

| Total: | 37.1 | 60.7 |

Source: Government decree #50, 2010. Most (RUR 9.5 billion) of the funding for SVBR was to be from "other sources" than the state budget, and it has now been dropped.

In March 2018 the FTP2010 was amended by the government in the light of reduced energy demand projections.

In December 2018 it was cancelled.

MBIR

Design of the 150 MWt multi-purpose fast neutron research reactor (mnogotselevoy issledovatilskiy reaktor na bystrych neytronach, MBIR) was finalized in 2014 by NIKIET and the equipment contract let to Atomenergomash-Technologies. Rostechnadzor issued a site licence in 2014, a construction licence in May 2015, and construction started in September 2015 at the Research Institute of Atomic Reactors (RIAR or NIIAR) in Dimitrovgrad, as part of the Nuclear Innovation Cluster there. The total project cost was then quoted as RUR 40-41 billion, with some of this expected from investors, and completion was scheduled for 2020. However, the project was paused shortly after construction began. In November 2020 Rosatom appointed a new contractor, AO Institut Orgenergostroy, and construction resumed, with commissioning now expected in 2027.

The MBIR will be a multi-loop research reactor capable of testing lead, lead-bismuth and gas coolants as well as sodium, and running on MOX fuel. Initially it will be sodium-cooled. It will be part of an international research centre at RIAR’s site and the IAEA was expected to sign an agreement on the MBIR International Research Centre in September 2016. The project is open to foreign collaboration, in connection with the IAEA INPRO programme. In April 2017 Rosatom was soliciting Japanese involvement. The MBIR will replace the BOR-60 fast research reactor. See also R&D section in the information page on Russia's Nuclear Fuel Cycle.

In January 2023 the reactor vessel for the MBIR was set in place marking the last major installation that requires the building to have an open top, with the next step being the construction of the reactor building dome. In August 2024 the first batch of pilot fuel elements for MBIR were produced. Installation of primary circuit equipment began in 2025.

Proryv (Breakthrough) project

The Proryv project is to create a new generation of nuclear power technologies on the basis of a closed nuclear fuel cycle using fast neutron reactors. This is proceeding as a high priority in nine coordinated centres.

The basic concepts include elimination of severe reactor accidents, closing the fuel cycle, low-activity radioactive waste, non-proliferation, reduced capital cost of fast reactors.

The nine responsibility centres include:

- Reprocessing technology and radioactive waste management for the reprocessing module (RM) of the pilot demonstration energy/power complex (PDEC or PDPC).

- Pilot production lines for onsite nuclear fuel cycle, including the fabrication/refabrication module (FRM) and the fast reactor used fuel reprocessing module (RM).

- Development of fuel elements and assemblies with mixed nitride uranium plutonium (MNUP) fuel, at Bochvar National Research Institiute (VNIINM).

- Building and operating the BREST-OD-300 reactor, at JSC NIKIET.

- Development of materials for the BN-1200 fast reactor, at JSC Afrikantov OKBM.

- Design engineering the pilot demonstration energy/power complex (PDEC or PDPC) including nitride fuel fabrication and recycling, and developing an industrial energy complex (IEC).

Most of these initiatives are more fully described in the companion page on Russia's Nuclear Fuel Cycle. BREST and BN-1200 are described below under Reactor Technology.

Floating nuclear power plants

Rosatom was planning to build seven or eight floating nuclear power plants (FNPPs) by 2015. The first of them was to be constructed and then remain at Severodvinsk with intended completion in 2010, but plans changed. Each FNPP was to have two 35 MWe KLT-40S nuclear reactors. (If primarily for desalination this set-up is known as APVS-80.)

A decision to commit to building a series was envisaged to be in 2014 when the first was expected to be near commissioning. Rosenergoatom earlier signed an agreement with JSC Kirov Factory to build further units, and Kirov subsidiary Kirov Energomash was expected to be the main non-nuclear contractor on these.

The keel of the first floating nuclear power plant (FNPP), named Akademik Lomonosov, was laid in April 2007 at Sevmash in Severodvinsk, but in August 2008 Rosatom cancelled the contract (apparently due to the military workload at Sevmash) and transferred it to the Baltiysky Zavod shipyard at St Petersburg, which has experience in building nuclear icebreakers. After signing a new RUR 9.98 billion contract in February, new keel-laying took place in May 2009. The 21,500 tonne hull (144 metres long, 30 m wide) was launched at the end of June 2010.

Completion and towing to the site had been expected in 2012 and grid connection in 2013, but due to insolvency of the shipyard JSC Baltijsky Zavod* and ensuing legal processes it was delayed considerably. Barely any work was done over 2011-12 after some RUR 2 billion allocated to finance the construction apparently disappeared. The state-owned United Shipbuilding Corporation acquired the shipyard in 2012 and a new contract with Baltijsky Zavod-Sudostroyeniye (BZS), the successor of the bankrupt namesake, was signed in December 2012. The cost of completing the FNPP was then put at RUR 7.631 billion.

* a subsidiary of privately-owned United Industrial Corporation.

Earlier at the end of 2012 the Ministries of Defence, Energy and Industry agreed to make Pevek the site for the first FNPP unit, the Academician Lomonosov. Vilyuchinsk, Kamchatka peninsula, was the site originally planned for its deployment to ensure sustainable electricity and heat supplies to the naval base there. Pevek on the Chukotka peninsula in the Chaun district of the far northeast, near Bilibino, was originally planned as the site for the second FNPP, to replace the Bilibino nuclear plant and a 35 MWe thermal plant as a major component of the Chaun-Bilibino industrial hub. Rosenergoatom said that the tariff revenue of Chukotka made it more attractive than the Vilyuchinsk naval base.

The two KLT-40S reactors from OKBM Afrikantov were installed in October 2013. The KLT-40S is a version of the icebreaker reactor for floating nuclear power plants which runs on low-enriched uranium (<20%) and hence has a bigger core and shorter refuelling interval: 3-4.5 years. Operational lifetime is 40 years.

In September 2015 Rosatom signed a cooperation agreement with the government of the Chukotka Autonomous District for power sector development around the Chaun-Bilibino Energy Hub, including installation of the first FNPP at Pevek. Construction of onshore facilities for the plant commenced in September 2016.

Total estimated costs for Pevek increased to RUR 37 billion at May 2015, partly due to factoring in the required site works and infrastructure. The government contributed to coastal infrastructure, with RUR 5 billion over 2016-20. Rosenergoatom said the pilot FNPP was costing Rosenergoatom RUR 21.5 billion, and it expects the second one to be about RUR 18 billion.

Mooring tests started in mid-2016, and in May 2018, the vessel completed the first leg of its journey to Pevek, mooring in Murmansk for fuel loading*. Fuel loading was completed in October 2018, with startup in December 2019, and commercial operation in May 2020. The plant is connected to the region's grid, heat and water supply.

* The Law of the Sea does not address non-propelled nuclear power plants at sea, so concerns by neighbouring countries en route cannot be resolved if reactors are commissioned before they are back in Russian waters

The third site for FNPP deployment was to be Chersky or Sakha in Yakutia. As of early 2009, four floating plants were designated for northern Yakutia in connection with the Elkon uranium mining project in southern Yakutia, and in 2007 an agreement was signed with the Sakha Republic (northeast Yakutia region) to build one of them, using smaller ABV-6* reactors. Five were intended for use by Gazprom for offshore oil and gas field development and for operations on the Kola peninsula near Finland and the Yamal peninsula in central Siberia. The draft energy plan released in September 2024 by UES showed that two land-based RITM units (RITM-200N) are now planned at Yakutia instead.

* The small Russian ABV-6M integral PWR is 16-45 MW thermal. A design known as the Volnolom FNPP consists of a pair of reactors (12 MWe in total) mounted on a 97-metre, 8700 tonne barge plus a second barge for reverse osmosis desalination (over 40,000 m3/day of potable water).

Earlier in July 2017 Rosatom announced the second generation of FNPPs, now called optimized floating power units (OFPUs), would use two RITM-200M reactors derived from those for the latest icebreakers. These are more powerful than the KLT-40S reactors, at 50 MWe each, have fuel enriched to almost 20%, need refuelling only every 10-12 years at a service base, so no onboard used fuel storage is required. Also, the actual reactors are lighter, so the barge is smaller* and displacement is reduced from about 21,000 to 12,000 tonnes. Operational lifetime is 40 years, with possible extension to 60 years.

* Apparently 115m long and 25m wide.

Rosatom is planning four OFPUs hosting eight RITM-200 units at Cape Nagloynyn to supply 440 MWe to the Baimskaya copper mining project south of Bilibino and Pevek. One OFPU will be held in reserve to cover refuelling and maintenance downtime. In September 2021 Rosatom subsidiary FSUE Atomflot and KAZ Minerals subsidiary GDK Baimskaya LLC signed an agreement for electricity supply from four 106 MWe OFPUs. The Rosatom commitment is over RUR 150 billion ($2.1 billion) and the electricity price is RUR 6.45/kWh (¢8/kWh) indexed for inflation. In September 2021 Rosatom awarded a $226 million contract to Wison (Nantong) Heavy Industries in China for the first two 19,100 tonne barge hulls. The reactors and turbines from Atomenergomash will be installed in Russia, at Baltijsky Zavod Shipbuilding in St Petersburg, where the other two barge hulls will be built (that shipyard is committed to building LK-60 icebreakers). In early September 2022 Atomenergomash signified the start of full construction of the first of four OFPUs through a keel laying ceremony.

As well as FNPPs, NIKIET is developing a sunken power plant which will sit on the sea bed supplying electricity for Arctic oil and gas development. This is SHELF, a 6 MWe integral PWR. NIKIET has also proposed its use for the RUR 100 billion Pavlovsky lead-zinc mine project in northern Novaya Zemlya. See also R&D section in the information page on Russia's Nuclear Fuel Cycle.

Export potential

In May 2014 the China Atomic Energy Authority (CAEA) signed an agreement with Rosatom to cooperate in construction of floating nuclear cogeneration plants for China offshore islands. These would be built in China but be based on Russian technology, and possibly using Russian KLT-40S reactors. This arrangement appears to have been displaced by indigenous Chinese developments. In August 2015 Rosatom and Indonesia’s BATAN signed a cooperation agreement on construction of FNPPs, but nothing further has been announced.

In June 2024 the Republic of Guinea and Rosatom signed an MOU to cooperate on the development of floating power units to supply electricity in the African country.

Heating

From the 1970s there have been plans for nuclear district heating plants (AST). The AST-500 integral PWR-type plant was designed by OKBM and built by Atommash, with the first one installed at Gorky and ready to start up in September 1989. However, local opposition prevented its operation. (Gorky is now Nizhny Novgorod.)

In the 1990s, 5 GW of thermal power plants (mostly AST-500 integral PWR type) were planned for district and industrial heat to be constructed at Arkhangelsk (four VK-300 units commissioned to 2016), Voronezh (two AST-500 units 2012-18), Saratov, Dimitrovgrad and (small-scale, KLT-40 type PWR) at Chukoyka and Severodvinsk. Also the main Russian nuclear plants were expected to provide 30.8 PJ cogeneration district heating by about 2010. (A 1000 MWe reactor produces about 95 PJ per year internally to generate the electricity.)

A RUTA-70 low-temperature 20-70 MWt pool-type district heating reactor has been designed by NIKIET and proposed for Obninsk. It would operate at atmospheric pressure and would have a subsidiary function as a neutron source for the Institute for Physics and Power Engineering (IPPE) or for desalination by MED – but has evidently not proceeded.

In 2016 four Russian cities expressed an interest in using small reactors to supply heat and power, according to NIKIET. A specific feasibility study was undertaken for an Arkhangelsk nuclear cogeneration plant. A broader Rosatom feasibility study on regional power concluded that up to 38 cogeneration reactors could be deployed at 14 sites for this purpose: Arkhangelsk (4, with high local support), Ishevsk (2), Ivanovo (2), Kazan (3), Khabarovsk (4), Komsomolsk-on-Amur (3), Kurgan (2), Murmansk (2), Perm (2), Tver (2), Ufa (2), Ulyanovsk (3), Vyatka (2) and Yaroslavl (3).

The basic cogeneration plant proposed by NIKIET is twin VK-300 units each rated 250 MWe, or 150 MWe plus 1675 GJ/h, conservatively to give joint annual output of 3 TWh and 16 PJ very competitively.

Many operating nuclear power plants in Russia provide district heat supply.

Heavy engineering and turbine generators

Atomenergomash (AEM) under Rosatom now claims to be the leading company in Russia for major components of nuclear power plants, controlling over 40 facilities and to be the sole Russian source of steam generators and primary coolant pumps for nuclear plants. AEM-Technology has two main plants: Petrozavodskmash in Karelia and Atommash at Volgadonsk. Atommash has a 15,100-tonne press and is producing reactor pressure vessel forgings for VVER-TOI reactors.

OMZ subsidiary Izhorskiye Zavody produces forgings for nuclear reactors including reactor pressure vessels, steam generators, and heavy piping. In 2008 the company rebuilt its 12,000 tonne hydraulic press, claimed to be the largest in Europe, and a second stage of work increased that capacity to 15,000 tonnes.

In May 2012 Rosenergoatom said that reactor pressure vessels for its VVER-TOI reactors would be made by both Izhorskiye Zavody and the Ukrainian works Energomashspetsstal (EMSS) with Russian Petrozavodskmash. Since then Atommash has also been producing pressure vessel forgings for VVER-TOI reactors. In mid-2015 Rosatom announced that a new nickel-alloy steel coupled with larger (4.2m) diameter pressure vessel would mean that the VVER-TOI should have a 120-year operational life. A 420-tonne ingot had been forged into one of these by OMZ-Spetsstal in December 2014. The new alloy was developed at Atomenergomash’s Central Research Institute for Machine Building Technology (CNIITMASH). However the pressure vessel for Kursk II-1 delivered to the site by Atommash in September 2021 is made of nickel-free steel, to give a service lifetime of 100 years.

Petrozavodskmash makes steam generators and had the contract for RPV and various internals for the (now abandoned) Baltic 1 reactor. Izhorskiye Zavody was expected to supply these components for unit 2.

ZiO-Podolsk also makes steam generators, including those for Belene/Kozloduy 7.

Turbine generators for the new plants are mainly from Power Machines (Silovye Mashiny – Silmash) subsidiary LMZ.

Turbine Technology AAEM is a joint venture of Atomenergomash and GE producing low-speed turbines based on Alstom's Arabelle design, sized from 1200 to 1800 MWe, with GE generators. It produces the Arabelle units at AEM's Atommash plant at Volgodonsk, most recently for Akkuyu in Turkey and El Dabaa in Egypt.

Ukraine's Turboatom is offering a 1250 MWe low-speed turbine generator for the VVER-TOI. Rosenergoatom says it insists on having at least two turbine vendors, and prefers three.

Reactor technology

Pressurized water reactors

VVER-1000, AES-92, AES-91

The main reactor design deployed until now has been the V-320 version of the VVER-1000 pressurized water reactor with 950-1000 MWe net output. It is from OKB Gidropress (Experimental Design Bureau Hydropress), has 30-year basic design life and dates from the 1980s. A later version of this for export is the V-392, with enhanced safety and seismic features, as the basis of the AES-92 power plant. All models have four coolant loops, with horizontal steam generators. Maximum burn-up is 60 GWd/tU. VVER stands for water-cooled, water-moderated energy reactor.

Advanced versions of this VVER-1000 with western instrument and control systems are being built at Tianwan in China and are being built at Kudankulam in India – as AES-91 and AES-92 nuclear power plants respectively. The former was bid for Finland in 2002 and for Sanmen and Yangjiang in China in 2005, while the AES-92 was accepted for the now-cancelled Belene project in Bulgaria in 2006. These have 40-year design life. (Major components of the two designs are the same except for slightly taller pressure vessel in AES-91, but cooling and safety systems differ. The AES-92 has greater passive safety features – 12 heat exchangers for passive decay heat removal; the AES-91 has extra seismic protection. The V-428 in the AES-91 is the first Russian reactor to have a core-catcher, V-412 in AES-92 also has core catcher.)

VVER-1200, AES-2006, MIR-1200

Development of a third-generation standardized VVER-1200 reactor of about 1170 MWe followed, as the basis of the AES-2006 power plant. Rosatom drew upon Gidropress, OKBM, Kurchatov Institute, Rosenergoatom, Atomstroyexport, three Atomenergoproekt outfits, VNIINPP and others. Two design streams emerged: one from Atomproekt in St Petersburg with V-491 reactor, and one from Atomenergoproekt in Moscow with V-392M reactor.

The V-491 provides about 1170 MWe gross, 1085 net, and the V-392M provides about 1199 MWe gross, 1114 net, both from 3200 MWt, along with about 300 MWt for district heating. This is an evolutionary development of the well-proven VVER-1000/V-320 and then the third-generation V-392 in the AES-92 plant (or the AES-91 for Atomproekt version), with longer operational lifetime (60 years for non-replaceable equipment, not 30), greater power, and greater thermal efficiency (34.8% net instead of 31.6%). Compared with the V-392, it has the same number of fuel assemblies (163) but a wider pressure vessel, slightly higher operating pressure and temperature (329ºC outlet), and higher burn-up (up to 70 GWd/t). It retains four coolant loops. It can undertake daily load following down to 80% power. Refuelling cycle is up to 24 months. Core catchers filled with non-metallic materials are under the pressure vessel. Construction time for serial units is "no more than 54 months".

AES-2006 (Rosatom)

The lead units were built at Novovoronezh II (V-392M), starting operation in 2016, and at Leningrad II (V-491) in 2018. Both plants use Areva's (now Framatome) Teleperm safety instrument and control systems. Atomproekt’s Leningrad II with V-491 reactor was quoted as the reference plant for the VVER units now operating at Tianwan in China. The two types of AES-2006 plant are very similar apart from the configuration of the safety systems. They are expected to run for 60 years with capacity factor of 92%, and with Silmash turbine generators. They have enhanced safety including that related to earthquakes and aircraft impact with some passive safety features and double containment. However, it appears that only six will be built domestically – two V-392M and four V-491 – before moving onto the VVER-TOI, with potential for international design certification.

For the Novovoronezh V-392M units Atomernergoproekt Moscow has installed what it calls dry protection, a 144-tonne structure surrounding the reactor core that reduces emission of radiation and heat. It consists of a steel cylinder with double walls, 7m diameter, with the space between them filled with specially formulated concrete. This gives it better aircraft crash resistance than V-491. They have passive decay heat removal by air circulation.

Atomproekt’s Leningrad V-491 units have four trains of active safety systems, with water tanks high up in the structure to provide water cooling for decay heat, and is more suited to Finland and central Europe rather than seismic sites (DBGM is only 250 Gal). Atomproekt’s AES-2006 has two steam turbine variants: Russian Silmash high-speed version for Russia, or Alstom Arabelle low-speed turbine as was proposed for Hanhikivi and MIR-1200.

For Europe, the basic Atomproekt V-491 St Petersburg version has been slightly modified by Atomproekt as the MIR-1200 (Modernized International Reactor), and bid for Temelin 3&4. It was also selected for Hanhikivi in Finland, as AES-2006E, with "extended list of accidents and external impacts" including higher seismic tolerance.

Atomstroyexport differentiates the VVER-1200M at Novovoronezh and for Rooppur from the VVER-1200E in Belarus. The differences are in the structure and layout of the safety systems.

VVER-1300, VVER-TOI

A further evolution, or finessing, of Moscow Atomenergoproekt’s version of the AES-2006 power plant with the V-392M reactor is the VVER-TOI (typical optimized, with enhanced information) design for the AES-2010 plant, the VVER-1300 reactor being designated V-510 by Gidropress. Rosatom says that this is planned to be standard for new projects in Russia and worldwide, with minor variations (such as the cheaper VVER-1300A). It has an upgraded pressure vessel with four welds rather than six, and will use a new steel which “removes nearly all limitations on RPV operation in terms of radiation embrittlement of metal”, making possible a service life of more than 60 years with 70 GWd/t fuel burn-up and 18 to 24-month fuel cycle. It has increased power to 3312 MWt, 1255 MWe gross (nominally 1300), improved core design still with 163 fuel assemblies to increase cooling reliability, larger steam generators, further development of passive safety with at least 72-hour grace period requiring no operator intervention after shutdown. It targets lower construction and operating costs, and 40-month construction time. It is claimed to require only 130-135 tonnes of natural uranium (compared with typical 190 tU now) per gigawatt year. It will use a low-speed turbine-generator. It can undertake daily load following down to 50% thermal power, ramping up at 1%/minute and down at 3%/minute, and has significant frequency control capability compared with AES-2006 reactors.

The project was initiated in 2009 and the completed design was presented to the customer, Rosenergoatom at the end of 2012. The design aim was to try and save 20% of the cost. It was submitted to Rostechnadzor in 2013 for licensing, and was certified by the European Utility Requirements for LWR Nuclear Power Plants (EUR) organization in 2019. EUR approval is seen as basic in many markets, notably China.

The first units are under construction at Kursk. In June 2012 Rosatom said it would apply for VVER-1200 design certification in UK and USA, through Rusatom Overseas, with the VVER-TOI version, but this did not proceed. Development involved OKB Gidropress (chief designer), NRC Kurchatov Institute (scientific supervisor), All-Russian Scientific and Research Institute for Nuclear Power Plant Operation (VNIIAES – architect-engineer), and NIAEP-ASE jointly with Alstom (turbine island designer). V-509 and V-513 reactors are variants of V-510, the V-513 as VVER-1300.

VVER-1300A

This is presented as a cheaper variant of the VVER-TOI/V-510 reactor, and has two new PGV-1300A steam generators, decreased metal content and decreased containment diameter. It is proposed as a variant of the VVER-TOI.

VVER-600

Since 2008 OKB Gidropress with SPb AEP and Kurchatov Institute has also been developing a two-loop VVER-600 (project V-498) from V-491 (1200 MWe, four-loop), using the same basic equipment but no core catcher (corium retained in RPV), as a Generation III+ type. In December 2011 Gidropress signed a contract with the Design and Engineering Branch of Rosenergoatom for R&D related to the VVER-600 reactor, though this was not then part of any federal Rosatom program. Gidropress presented the design to Rosenergoatom in February 2013, saying a project package could be ready in two years. It will be capable of load-following, and would have a 60-year life. Rosenergoatom has been considering it for the Baltic plant site as a straightforward option to replace the 1200 MWe units, and it is now planned for Kola. It has high export potential, and Gidropress, NIAEP and Kurchatov have been progressing it slowly. The VVER-600 supercedes the VVER-640 in Gidropress plans,* and Rosatom envisages its deployment in 2020s.

* The VVER-640 (V-407), an 1800 MWt, 640 MWe design originally developed by Gidropress jointly with Siemens. It had advanced safety features (passive safety systems). After apparently beginning construction of the first at Sosnovy Bor, funds ran out and it disappeared from plans. However, it came back on the drawing boards, now as a Generation III+ type, with four cooling loops, low power density, low-enriched fuel (3.6%), passive safety systems, 33.6% thermal efficiency and only 45 GWd/t burn-up. In March 2013 SPbAEP (merged with VNIPIET to become Atomproekt) said that subject to Rosatom approval it could have a VVER-640 project ready to go possibly at the Kola site by the end of 2014. The project partners – Atomenergomash, OKB Gidropress, Central Design Bureau for Marine Engineering (CDBME) of the Russian Shipbuilding Agency, OMZ’s Izhorskiye Zavody, Kurchatov Institute, and VNIPIET – “confirmed its readiness for updating aiming at commercialization.” In May 2013 Atomenergoproekt said it has already been discussing with VNIPIET the feasibility and practicability of using the VVER-640 project “as the starting point for the development of next-generation medium-power nuclear power plants, including with the use of passive safety systems.”

VVER-1500

About 2005 Rosatom (the Federal Atomic Energy Agency) promoted the basic design for VVER-1500 pressurized water reactors by Gidropress as a priority. Design was expected to be complete in 2007, but the project was shelved in 2006. It was a four-loop design, 42,350 MWt producing 1500 MWe gross, with increased pressure vessel diameter to 5 metres, 241 fuel assemblies in core enriched to 4.4%, burn-up up 45-55 and up to 60 GWd/t and life of 60 years.

VVER-1800

This is a development of the VVER-1300A, but with three loops, using steam generators and circulation pumps from it, and reactor pressure vessel and internals from VVER-1500, which it supercedes. However, development is paused.

VVER-SKD-1700

A Generation IV Gidropress project in collaboration with the Generation IV International Forum is the supercritical VVER (VVER-SKD or VVER-SCWR) with higher thermodynamic efficiency (45%) and higher breeding ratio (0.95) and oriented towards the closed fuel cycle. Focus is on structural materials and fuels. The main version is 3830 MWt, 1700 MWe, with 540°C operating temperature. The SPA Central Research Institute of Machine Engineering Technology (TsNIITMASH) in Moscow and OKB Giidropress are involved in the draft proposals. OKB Gidropress says that “Such reactors are expected to increase significantly thermal energy conversion efficiency, move to the fast neutron spectrum in the reactor core and, by thus, substantially improve parameters of breeding of the secondary nuclear fuel in the reactor.” Also referred to as VVER-1700, V-393. Rosatom is reported to be developing it to a full design and bidding to build a prototype ahead of other SCWR designs in Europe, Canada, China and Japan.