Nuclear Power in the European Union

- The EU depends on nuclear power for about one-quarter of its electricity, and a higher proportion of base-load power. Nuclear provides about half the low-carbon electricity.

- Very different energy policies pertain across the continent and even within the EU, but attention is now being given to an EU energy union.

- A substantial degree of transmission interconnection exists in western Europe, but much more investment is needed.

- Electricity markets are a key to the future of reliable generation capacity, including nuclear.

NB please consult individual country pages for country-specific details; this page only provides an overview.

The European Union (EU) comprises 27 countries across continental Europe which are committed to working together and sharing unrestricted trade. Since six countries founded it in 1958 as the European Economic Community free trade area, it has acquired more members, and in 1993 its name became the European Union (EU). The UK joined in 1973 but left in January 2020 following a national referendum in 2016 on its membership. In the 1980s and 1990s it gained political substance as members transferred some powers to it, and it increasingly became characterized by regulation, including of energy. The former East Germany was admitted as part of reunified Germany in 1990. A number of treaties agreed by member states define these central powers wielded from Brussels. The total EU population is approximately 450 million.

The non-EU European countries of Switzerland, Norway, the United Kingdom and some Balkan states* are to some extent electrically networked with the EU. Norway participates in the EU Emissions Trading System. In March 2022, following Russia's invasion, Ukraine's grid was synchronized with and connected to the European grid.

*Serbia, Bosnia & Herzegovina, Montenegro, Albania, North Macedonia

The European Parliament is directly elected from within each EU member state and can pass laws. The EU's broad priorities are set by the European Council, which brings together national heads of state and a rotating EU president. The interests of the EU as a whole are promoted by the European Commission (EC), whose members are appointed by national governments. The EC, based in Brussels, proposes legislation, and is then responsible for implementing it. Governments defend their own country's national interests in the EU Council.

In 2024 in the EU, 33% of electricity was generated from fossil fuels and biomass, 24% from nuclear, 28% from wind and solar, and 15% from hydropower.

EU energy policy, energy union

Member states of the EU have a wide range of views on the use of nuclear energy. As such EU level policies do not stipulate future deployment levels of nuclear technologies, unlike for renewables. The policies of countries in the EU with civil nuclear power plants are outlined in dedicated country profiles.

Since 2015, the EC has been implementing the energy union strategy. The energy union aims to integrate and strengthen the EU’s internal energy market, and its five priorities are: enhance security of energy supply; build a single integrated energy market; increase energy efficiency; decarbonize the economy; and boost research and innovation.

However, two developments are cutting across the single electricity market concept, both related to ensuring that critical future demand can be met: national capacity markets; and demand response markets. France, Italy, Spain, Portugal, Italy, Greece and Ireland all offer capacity payments of some sort, which are often costly, distort the market, and run counter to the idea of phasing out fossil fuel subsidies in the long term.

In November 2016 the EC proposed the EU Clean Energy Package, a set of eight legislative proposals designed to implement the energy union strategy. The legislative acts, adopted 2018-2019, set ambitious targets for energy efficiency, renewable energy and emissions reductions by 2030. The package also removed priority dispatch for new renewables capacity. EU energy regulators European Union Agency for the Cooperation of Energy Regulators (ACER) and the Council of European Energy Regulators (CEER) in May 2017 called for its removal for existing renewable energy capacity as well, in order to avoid the "perverse outcome" of inefficient old plant continuing to operate, adding to system costs. In Germany, many wind projects had started to approach 20 years of operation, with decisions needing to be made on operating lifetime extension, or closure or repowering. ACER and CEER also called for removal of the 90% compensation floor for renewable energy curtailment, making the approach to redispatch and curtailment less prescriptive, with market-based prices being the basis for compensation for renewable energy plants.

In December 2019 the EC created the European Green Deal, which pledged to reduce greenhouse gas emissions in 2030 by 55% compared to 1990 levels, and that the EU would become climate neutral by 2050. These objectives became mandatory under the European Climate Law passed in June 2021. Proposals under the 'Fit for 55' package to bring EU energy and climate legislation in line with the pledge to reduce greenhouse gas emissions by 55% by 2030 were released in 2021 and in June 2022 the renewable energies directive and the energy efficiency directive were adopted by the European Council. These directives increased the binding targets for the share of energy from renewables to 40% (from 32%) by 2030, and to reduce projected final energy consumption in 2030 by 36% compared with 2007 levels.

Following the major impact on European energy supply from the war in Ukraine, the EC in May 2022 presented its REPowerEU Plan that aims to phase out dependence on Russian fossil fuels. It called for a further increase to targets for energy efficiency and renewables deployment by 2030.

Earlier in February 2021 a report commissioned by the European Conservatives and Reformists (ECR) and the Renew Europe groups of the European Parliament examined three issues key to the EU’s ambition to be climate neutral by 2050: the effect of EU climate neutrality on the average global atmospheric temperatures by 2050 and 2100; the spatial (land and sea) requirements for wind and solar energy compared with nuclear energy in the Czech Republic and the Netherlands; and the cost of wind/solar energy and of nuclear energy for these two countries. The study found that, in realistic scenarios, there is insufficient land to meet all the power demand of the Netherlands – "a country along the North Sea with abundant wind" – and the Czech Republic – "a landlocked country with no access to the sea and a geographically more challenging landscape" – if they were to rely solely or predominantly on wind and solar power. It also concluded that nuclear energy is more cost-effective than renewables. Even when major efficiency improvements in solar and wind farms are taken into account, nuclear energy would remain the cheaper option in 2050, it said.

In March 2023 the EC proposed electricity market reforms under the Net-Zero Industry Act to scale up manufacturing of clean technologies in the EU as part of the clean-energy transition. Under ‘advanced technologies’, small modular reactors (SMRs) were mentioned as one of the technologies that could make a significant contribution to decarbonization.

In October 2023 the EC agreed to include existing nuclear plants in the electricity market reforms. The agreement stipulated that governments may apply contracts for difference (CfDs) for investments aimed at extending the operating lifetimes of existing power plants, but these would be subject to specific “design rules” established by the EC to prevent market distortion. The reform was part of a wider reform of the EU's electricity market design which also included a regulation focused on improving the EU's protection against market manipulation.

In November 2023 the European Parliament approved the Net Zero Industry Act (NZIA) by a 376 to 139 vote. The NZIA sets a target for Europe to produce 40% of its annual deployment needs in net-zero technologies by 2030 and to capture 25% of the global market value for these technologies. Included in the ten proposed technologies was "advanced technologies to produce energy from nuclear processes with minimal waste from the fuel cycle, small modular reactors, and related best-in-class fuels."

EU nuclear generation capacity

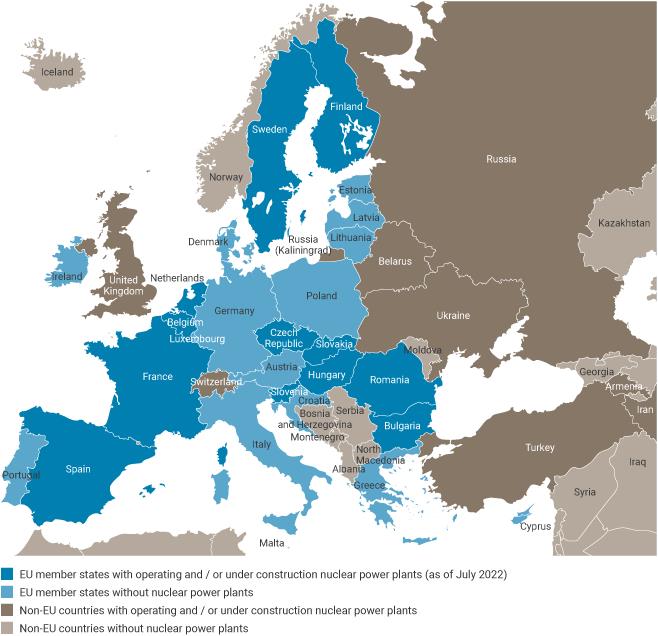

The 100 nuclear power reactors (98 GWe) operating in 12 of the 27 EU member states account for about one-quarter of the electricity generated in the whole of the EU. Over half of the EU’s nuclear electricity is produced in only one country – France. The 66 units operating in five non-EU countries (United Kingdom, Belarus, Russia, Ukraine and Switzerland) account for just over 30% of the electricity in the rest of Europe. Norway and Switzerland are effectively part of the EU synchronous grid (see later section on Interconnection: European Transmission Infrastructure).

Nuclear energy in the EU is governed to a large extent by the Euratom Treaty, which was one of the founding treaties establishing the EU. All EU member states are party to it by default. The European Atomic Energy Community (Euratom) was established in March 1957 and associated with the Treaties of Rome in 1958 to form a common market for the development of the peaceful uses of atomic energy (see below).

The Euratom Treaty requires the EC to periodically issue a nuclear illustrative programme (PINC), based on data from member states, and the latest of these was published in May 2017 (the first since 2007). It forecast a decline in EU nuclear capacity to 2025 and then a levelling out to 2050 at 95-105 GWe. This scenario would require €45 to €50 billion to be invested in long-term operation programmes and €350 to €450 billion in new reactors by 2050, as well as expenditure on decommissioning and waste management. The projected total nuclear costs to 2050 total €649 to €755 billion. This compares with the required investment of between €3.2 trillion and €4.2 trillion in the overall EU energy supply to 2050 in order to meet the objectives of the energy union strategy.

Although the establishment and operation of power generating capacity is undertaken on a national basis, a lot of electricity trading is undertaken across national boundaries in the EU, and any country’s energy policies have significant implications for neighbours. While economic considerations are normally paramount, energy policies relating to carbon emissions, energy security or ideology may trump economics and skew the choice of generating technology.

Although nuclear is a proven source of low-carbon, dispatchable electricity giving a high degree of energy security and provides 40% of the EU’s carbon-free electricity, the sector today faces major challenges within the EU. Some member states are strongly anti-nuclear, and electricity markets are often structured in response to populist support for renewables. In the period to 2030, nuclear capacity that will be lost due to the closure of a number of reactors – either because they have reached the end of their operating lifetimes or due to political interference – is expected to outweigh that gained from new reactors. A slight decrease from the current EU nuclear capacity is therefore expected in the near term.

Nuclear plant construction is currently under way in only two EU member states – France and Slovakia. These construction projects have experienced cost overruns and delays. Further new units likely to come online within the next 15 years are outlined in the table below. The long-term future of nuclear power in the EU is likely to depend on the outcome of these projects, which are relatively few in number – in total less than planned in Russia.

EU nuclear power

|

COUNTRY |

|

|

|

|

|

|

||||||

| TWh | % | No. | MWe | No. | MWe | No. | NWe | No. | MWe | tonnes U | ||

| Belgium |

31.3 |

41.2 |

4 |

3463 |

0 |

0 |

0 |

0 |

0 |

0 |

516 |

|

| Bulgaria |

15.5 |

40.4 |

2 |

2006 |

0 |

0 |

2 |

2300 |

0 |

0 |

334 |

|

| Czech Republic |

28.7 |

40.0 |

6 |

4212 |

0 |

0 |

1 |

1200 |

3 |

3600 |

715 |

|

| Finland |

32.8 |

42.0 |

5 |

4369 |

0 |

0 |

0 |

0 |

0 |

0 |

616 |

|

| France |

323.8 |

64.8 |

57 |

63,000 |

0 |

0 |

0 |

0 |

6 |

9900 |

8232 |

|

| Germany |

6.7 |

1.4 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

| Hungary |

15.1 |

48.8 |

4 |

1916 |

0 |

0 |

2 |

2400 |

0 |

0 |

320 |

|

| Netherlands |

3.8 |

3.4 |

1 |

482 |

0 |

0 |

0 |

0 |

2 |

2000 |

69 |

|

| Poland |

0 |

0 |

0 |

0 |

0 |

0 |

3 |

3750 |

26 |

10,000 |

0 |

|

| Romania |

10.3 |

18.9 |

2 |

1300 |

0 |

0 |

2 |

1440 |

6 |

462 |

185 |

|

| Slovakia |

17.0 |

61.3 |

5 |

2308 |

1 |

471 |

0 |

0 |

1 |

1200 |

527 |

|

| Slovenia |

5.3 |

36.8 |

1 |

688 |

0 |

0 |

0 |

0 |

1 |

1200 |

127 |

|

| Spain |

54.4 |

20.3 |

7 |

7123 |

0 |

0 |

0 |

0 |

0 |

0 |

1218 |

|

| Sweden |

46.6 |

28.6 |

6 |

7008 |

0 |

0 |

2 |

2500 |

0 |

0 |

932 |

|

In the non-EU neighbouring countries the outlook is more positive for nuclear, both in the near term and longer term. Construction is now under way in Russia, Belarus and Turkey using VVER technology, and in the United Kingdom, where two EPR reactors are being built at Hinkley Point.

EU neighbours nuclear power

|

COUNTRY |

|

|

|

|

|

|

||||||

| TWh | % | No. | MWe | No. | MWe | No. | NWe | No. | MWe | tonnes U | ||

| Belarus |

11.0 |

28.6 |

2 |

2220 |

0 |

0 |

0 |

0 |

0 |

0 |

357 |

|

| Russia |

204.0 |

18.4 |

36 |

26,802 |

7 |

5290 |

13 |

7650 |

51 |

48,261 |

5436 |

|

| Switzerland |

23.4 |

32.4 |

4 |

2973 |

0 |

0 |

0 |

0 |

0 |

0 |

412 |

|

| Turkey |

0 |

0 |

0 |

0 |

4 |

4800 |

0 |

0 |

8 |

9600 |

882 |

|

| Ukraine † ‡ |

50.0 |

50.7 |

15 |

13,107 |

2 |

1900 |

2 |

2500 |

7 |

8750 |

1673 |

|

| United Kingdom |

37.3 |

12.5 |

9 |

5883 |

2 |

3440 |

2 |

3340 |

2 |

2300 |

817 |

|

† Under Construction figures include a number of units where construction is currently suspended: Khmelnitski 3&4 (Ukraine).

‡ Ukraine 2023 electricity generation estimated.

EU Emissions Trading System

The EU has led the world in creating an emissions trading system (ETS) for carbon dioxide, which is the cornerstone of EU policy to counter climate change, and a major factor in EU energy policy. The ETS is a cap-and-trade system which is seen as providing the core of a wider scheme to limit carbon emissions worldwide. It works by setting a cap on greenhouse gas emissions from installations and reduces it each year in line with the so-called linear reduction factor (LRF).

The ETS aims to reduce Europe’s emissions to 55% below 1990 levels by 2030. It covers some 10,000 installations (power stations and industrial plants) in 27 EU countries plus Norway, Iceland and Liechtenstein accounting for nearly half of the EU’s carbon emissions. The emissions trading system of Switzerland has been linked to the EU ETS since September 2020. The United Kingdom left the ETS at the start of 2021.

After a positive start in 2005, in May 2006 the price of emissions allowances under the ETS for the first commitment period (2005-2007) plunged to less than half their previous value, indicating fundamental problems with the efficacy of the whole scheme. Attempts have been made since then to address those problems. In 2011, carbon to the value of about €112 billion was traded on the ETS, but in 2012 this dropped to about €75 billion, its lowest level since 2008.

In January 2014 the EC published its 2030 framework for climate and energy policies, including a legislative proposal for the ETS to establish a market stability reserve (MSR). The MSR was brought into operation in January 2019. It works by removing 24% of the supply of carbon allowances in circulation each year to support carbon prices.

The fourth trading phase of the ETS started in January 2021. From 2013-2020 the LRF was 1.74% per year. In the fourth phase (2021-2030) this increased to 2.2% under the 40% emissions goal. Under the EU ETS, certain businesses are provided free allocation of carbon allowances under the so-called 'carbon leakage list' – a group of sectors thought to be at highest risk of relocating to avoid the scheme. In the fourth trading phase the list of sectors eligible was cut from 180 to about 60.

The EU is looking at ways to expand the EU ETS to help deliver the bloc’s decarbonization goals. Currently the system covers slightly over 40% of Europe’s economy. In September 2020 the European Parliament voted to expand the system to include shipping.

Emissions reduction targets and means

The 2008 EC Climate and Energy Package set the '20-20-20' targets for 2020: a 20% reduction in greenhouse gas emissions from 1990 levels, a 20% renewables share in energy consumption and a 20% improvement in EU energy efficiency. The EC's 2030 framework for climate and energy policies published in January 2014 moved away from major reliance on renewables to achieve emissions reduction targets and allowed scope for nuclear power to play a larger role. It is focused on CO2 emissions reduction, not the means of achieving that, and allows more consideration for cost-effectiveness. However, disincentives to high CO2 emissions remain inadequate to drive change from high dependence on coal. This was debated and largely accepted in October 2014 by EU leaders by way of taking a lead in relation to the 2015 UN climate conference in Paris, and it set collective targets to reduce carbon dioxide emissions, raise efficiency and deploy more renewables (EC document SN 79/14).

The centrepiece of the 2030 framework is a 'binding' 40% reduction in domestic greenhouse gas emissions by 2030 (compared with a 1990 baseline) which will require strong commitments from EU member states. Current policies and measures if followed through should deliver a 32% reduction by then, so 40% “is achievable” and widely supported. It implies a 43% cut from 2005 for CO2 in sectors covered by the EU Emission Trading System (ETS) and 30% for the rest. The 40% EU target is to be broken down into 28 nationally-binding targets.

There were to be no post-2020 national renewables targets, leaving individual states free to use whatever technology they wish to achieve emission reductions in the longer term, though a 27% “headline target at European level for renewable energy” was included. In the October 2014 statement, renewables should be deployed to make up a total of 27% of EU energy by 2030 under another ‘binding’ target (in 2013 including hydro they comprised about 22%). However, these were evidently conditional upon the UN climate conference in December 2015 achieving comparable and legally-binding outcomes. A ‘flexibility clause’ was added to the final text, so that the EU Council “will revert to this issue after the Paris conference” and “will keep all elements of the framework under review”.

As noted above, the framework also proposed reform of the ETS with a new instrument to stabilize the market, to make it the principal driver of climate policy. It ratcheted down the maximum covered emissions from the EU by 2.2% per year from 2021 onwards, an increased rate of decarbonization compared with the 1.74% in the previous trading phase (2013-2020). An ‘indicative’ and non-binding target should raise energy efficiency by 27% against “projections of future energy consumption based on current criteria” and “delivered in a cost-effective manner”. In February 2017 the European Parliament voted in favour of the EC’s proposals. See also ETS section in Policy Responses to Climate Change paper.

Wind and solar in four EU countries, 2022

| Wind capacity end 2022, GWe | Wind output 2022, TWh | Solar capacity end 2022, GWe | Solar output 2022, TWh | |

| Germany | 58.1 | 125.3 | 66,5 | 60.8 |

| Spain | 29.8 | 62.8 | 19.1 | 34.8 |

| Italy | 11.5 | 20.6 | 25,1 | 28.1 |

| France | 20.9 | 38.1 | 17.1 | 20.6 |

Source: International Energy Agency

In January 2020 the EC unveiled its plan for at least €1 trillion in sustainable development investment over the next decade. The European Green Deal Investment Plan (EGDIP) is the 'investment pillar' of the Green Deal. Transition fund money under the plan will not finance construction of nuclear power plants, despite the fact that nuclear provides 50% of the EU's low-carbon electricity.

Earlier in May 2016 the EC confirmed that 2008 laws requiring member states to use “at least 10%” renewable energy in transport will be scrapped after 2020, dampening a protracted controversy surrounding the environmental damage caused by biofuels.

In eastern Europe outside the EU there are no corresponding carbon reduction policies.

Energy security

In May 2014 the European Commission proposed a new European Energy Security Strategy, in the context of its energy import dependency of more than 50%, with 39% of EU gas imports in 2013 coming from Russia. Diversifying external energy supplies, upgrading energy infrastructure, completing the EU internal energy market and saving energy are among its main points. Central to it is the urgent need for the EU to increase its indigenous energy production, improve transmission infrastructure and reduce its dependence upon external suppliers. The European nuclear industry role is vital to this strategy. The EC acknowledged that "electricity produced from nuclear power plants constitutes a reliable base-load supply of emission-free electricity and plays an important role for energy security," and that "EU industry has technological leadership on the whole chain, including enrichment and reprocessing." The EC recommended that the Euratom Supply Agency should be responsible for ensuring a diverse supply of nuclear fuel, both for the EU's current fleet of nuclear power plants and for those that are due to be built. Uranium, even though imported, represents a much lower effective dependence on external suppliers than coal or gas, since significant reserves can easily be held. Nuclear power is therefore classified as indigenous production.

Germany has its Energiewende policy involving phasing out nuclear power by 2023 and increasing its reliance on solar and wind power. Subsidies on these renewables are accompanied by giving them priority grid access, so that when they are producing they displace other sources from the grid. This reduces the load factors of gas, coal and nuclear plants, most critically in Germany but also in other places where these policies prevail to any degree. This compromises the economic viability of those plants, especially the newer ones which must earn money to repay construction costs. Coupled with this side effect from renewables’ grid priority is the low ETS carbon price and also low cost of coal, which makes coal-fired generation attractive. Despite concern about CO2 emissions, Germany remains one of the world's biggest consumers of coal. While gas plants fit better as back-up for expanded renewables, they are less economic than coal, and gas supplies are uncertain, especially since Russia's military offensive against Ukraine in 2022.

In May 2015 investment bank UBS published a report showing that the pace of closures in the coal and gas sector in Europe was accelerating – even as the growth in wind and solar renewables steadies and, in some countries, slows. According to its data, some 70 GWe of coal- and gas-fired generation had been shut down in the last five years, and the pace is increasing: 28 GWe in 2014, 27 GWe in 2013.

UBS said that the combination of reduced demand and yet more renewable energy additions over the next two years (47 GWe) will force the closure of at least 24 GWe of coal and gas capacity, and could lead to another 30 GWe of closures just to ensure that the remaining coal- and gas-fired plants can stabilize profits. At the moment nearly half of the remaining 260 GWe of coal- and gas-fired generation in Europe (38 GWe of it in Germany) is cash-flow negative, meaning they do not earn enough money to cover basic costs. UBS described the potential closure of so much at-risk capacity as a potential disaster that could leave the system precariously balanced, with not enough capacity to meet peak demand. The report showed total capacity of 908 GWe, with 30% of that coal and gas.

EY, a consultancy, calculates that utilities across Europe wrote off €120 billion of assets because of low power prices between 2010 and 2015, due to the structure of wholesale power prices. Wind and solar have a profound effect here, and investment in non-renewables remains very low. The more intermittent renewables there are in the system, the greater the effect on wholesale prices for dispatchable sources which become simply back-up.

In 2018 Euratom said that the EU had uranium inventories that could fuel EU utilities' reactors for three years. Euratom acknowledged that the average concealed a wide range, but stated that all utilities are covered for at least one year.

In February 2022, Russia launched a military offensive against Ukraine (see information page on Russia-Ukraine War and Nuclear Energy). A statement from the EC in June 2022 accused Russia of using natural gas as a “political and economic weapon.” The EU’s dependency on Russian gas imports has resulted in concerns over securing supply and a significant increase in wholesale energy prices. With concerns over energy supply for the winter, in May 2022, EU leaders convened and agreed to ban almost 90% of all Russian imports by the end of that year. Meeting again in June 2022, the EC adopted new rules to improve security of supply to the EU, with member states agreeing to “ensure their gas storage facilities are filled before winter” and “share storage facilities in a spirit of solidarity.” In July 2022, a voluntary political agreement to reduce natural gas demand by 15% for the winter was reached, and adopted in August.

Russian dependence

EU heads of state pledged in 2014 to focus on energy security and to agree on a climate and energy framework. They were divided on the impact of the Ukrainian crisis (Russian control of Crimea and subsequently parts of eastern Ukraine), with Germany calling for ambitious carbon emissions reductions, renewables and energy efficiency goals to lower the reliance on imported fossil fuels, notably Russian gas. Russia then supplied over 30% of Europe’s gas, and half of this transitted via Ukraine. However, Poland and other eastern European countries wish to maintain significant dependence on domestic energy resources such as coal and possibly shale gas as a higher priority than emissions reductions. Gazprom gas exports to western Europe increased by about 40% over 2010 to 2020.*

* EnergyMarketPrice 17/10/14 reported on an evaluation of the vulnerability of the (then) EU-28 and ten neighbouring countries to a possible six-month halt in gas supplies from Russia. It noted that Germany was Europe's main purchaser of Russian gas, paying Russian gas exporter Gazprom approximately $15 billion a year, while EU members such as Bulgaria and Slovakia were almost completely dependent on Russian gas imported through Ukraine. The article said that a halt in Russian supplies would be a peril to markets such as Bulgaria and Britain, since these countries had insignificant gas storage capacities, of three weeks and two months respectively. Meanwhile, Germany had reserves for almost half a year, or among the biggest in Europe.

Several Russian-designed nuclear power reactors get their fuel mainly from TVEL in Russia, and the older VVER-440 units depend wholly on TVEL for fuel fabrication. A lot of EU uranium enrichment and conversion is done in Russia, though other capacity is available in the EU and USA.

Russian nuclear reactors in the EU are in Bulgaria (2), Czech Republic (6), Finland (2), Hungary (4) and Slovakia (5, with one more being built). Hungary has an agreement for two more to be built. Finland was planning one with Russian equity, but the project has been cancelled.

Regarding nuclear fuel, the EC’s 2014 European Energy Security Strategy referred to above said specifically: "There is no diversification, nor back-up in case of supply problems (whether for technical or political reasons)." It went on to urge: "Ideally, diversification of fuel assembly manufacturing should also take place, but this would require some technological efforts because of the different reactor designs." Westinghouse produces some fuel for VVER-1000 reactors in Ukraine and Czech Republic, as well as VVER-400 fuel for Finland.

In early 2015 the EC and the Euratom Supply Agency disapproved a fuel supply contract between Rosatom and Hungary’s MVM for the planned Paks II VVER plant. The contract was later approved by Euratom after the duration of the exclusive contract with Rosatom was cut from 20 to 10 years, after which time alternative suppliers would be able to bid to supply fuel. The EC reiterated that diversification of nuclear fuel supply for Russian VVER reactors is very important to it.

In June 2015 the Euratom research and training programme, which is part of Horizon 2020, the EU's research and innovation programme, provided €2 million to Westinghouse and eight European partners "to establish the security of supply of nuclear fuel for Russian-designed reactors in the EU." This is part of a Euratom project, known as ESSANUF – European Supply of Safe Nuclear Fuel – and largely concerns fuel for 16 VVER-440 reactors. Westinghouse, with Enusa, had provided VVER-440 fuel for Loviisa in Finland over 2001 to 2007. The ESSANUF project was completed in March 2018.

Interconnection: European transmission infrastructure

More broadly than the EU, in May 2014 the power grids and exchanges in southern and north-western Europe were connected, covering about 70% of European customers and with annual consumption of almost 2400 TWh. The common day-ahead power market created through the physical and financial integration of the two regions extends from Portugal to Finland. This is expected to lead to a more efficient utilization of the power system and cross-border infrastructures, as a result of a better harmonization between energy markets. It is expected that electricity markets in the Czech Republic, Slovakia, Hungary and Romania will join similarly and then link to the rest of Europe. Poland is partially integrated with north-western Europe through a subsea line to Sweden. Italy's possible integration will depend on Switzerland's discussions with the European Union on connecting power systems.

In October 2014 EU leaders renewed a 2002 commitment to increase energy trading through electricity connectors to 10% by 2020, i.e. that much of each country’s generation capacity should be available for trade across borders. The statement said that "The integration of rising levels of intermittent renewable energy requires a more interconnected internal energy market and appropriate back up, which should be coordinated as necessary at regional level." The Baltic States, Portugal, Spain, and also Greece are priorities of electricity interconnection and integration.

In Europe, the power transmission system operating body ENTSO-E (European Network of Transmission System Operators for Electricity) comprising 41 transmission system operators (TSO) from 34 countries, has assessed the ability of Europe's grid networks to become a single internal energy market. This will require some €94 billion in new and upgraded power lines in order to meet the EU's renewables and energy market integration goals. It identified 100 power bottlenecks standing in the way, with 80% of them relating to the challenge of integrating renewable energy sources such as wind and solar power into national grids. One goal (set in 2002) is to have a level of interconnection for each country at least equivalent to 10% of its generating capacity, to achieve trans-EU electricity infrastructure. The EC proposes 15% interconnection by 2030, though this still needs to be defined.

In November 2015 the report from a 40-month e-Highway2050 study commissioned by the EC and involving the TSOs was released, to give a longer-term perspective on planning than provided by ENTSO-E’s ten-year network plans. The report says that Europe does not need the sort of long-distance HVDC network proposed a few years ago, but must attend to bottlenecks that need fixing by 2050. The 2030 grid plan from ENTSO-E will be insufficient to support any 2050 low-carbon future (80-95% cut in emissions). Depending on the scenario, the annual investment required is €10-20 billion per year, for an annual benefit of €14-55 billion. The expected benefits outweigh the costs in all the scenarios. Greater investments deliver proportionally greater benefits. However, the grid must relate to generation, which remains uncertain in several respects. A separate study commissioned by VGB PowerTech said that the historical rate of investment in thermal power plants must be maintained up to 2035 to back up variable renewables. Total generation investment needed amounts to about €40 billion per year to 2025, rising to €40-80 billion per year from 2030, and including gas turbines, nuclear plants and CCS. Security of supply needs to be a priority.

Much of the European investment needs to be on refurbishment or construction of about 51,000 km of extra high voltage power lines and cables, to be clustered into 100 major investment projects dealing with the main bottlenecks. "The fast and massive development of renewable energy sources drives larger, more volatile, power flows over longer distances across Europe and is responsible for 80 out of 100 identified bottlenecks," according to ENTSO-E’s 2012 Ten-Year Network Development Plan.

The TSOs said their analysis showed that extending the grid by only 1.3% enables the addition of 3% generation capacity and the integration of 125 GWe of renewable energy sources – all at a cost of 2 cents per kilowatt-hour for electricity consumers over a 10-year span. "Cumbersome permit-granting procedures and a lack of public acceptance for power lines are presently the most relevant obstacles" facing the efforts. Hence ENTSO-E proposed that each EU member state should designate a single competent authority responsible for the completion of the entire permit-granting process, which would not exceed three years.

By 2017 new power system operation rules were in force across the EU. These include capacity allocation across ten regions, congestion management, and grid connection nodes. Rules on emergency restoration and balancing were being finalized.

Another goal of the EU's grid infrastructure efforts is reducing the 'energy island' status of Italy, Iberian Peninsula, Ireland and Baltic states. This will be addressed by the upgrades, while reducing the total generation costs by about 5%. Lithuania’s revised energy policy in 2012 involved rebuilding the grid to be independent of the Russian system and to integrate with the ENTSO-E synchronous system, as well as strengthening interconnection among the three Baltic states (see further details of transmission developments in Baltic states in the information paper on Electricity Transmission Grids).

This EU integration was an important factor leading to Russia suspending work on its new Baltic nuclear power plant in its exclave of Kaliningrad after 14 months' construction on the first of two planned 1200 MWe units. It was designed for the EU grid. Despite endeavours to bring in west European equity and secure sales of power to the EU through proposed transmission links, the plant is isolated, with no immediate prospect of it fulfilling its intended purpose. Kaliningrad has a limited transmission link to Lithuania, and none to Poland, its other neighbour. Both those countries declined to buy output from the new Baltic plant. Lithuania does not wish to upgrade its Kaliningrad grid connection to allow power from the Baltic nuclear plant to be sent through its territory and Belarus to Russia. As well as upgrading the Lithuania link, Russian grid operator InterRAO had plans to build a 600-1000 MWe link across the Kaliningrad border to Poland and a 1000 MWe HVDC undersea link to Germany, but with no customers these plans are not proceeding. In March 2013 Rosatom said that Russia had applied for Kaliningrad to join the EU grid system (ENTSO-E), evidently without response.

Electricity markets in the EU are a key to the survival of reliable, especially base-load, capacity. Preferential access to the grid by subsidized renewable sources depresses wholesale prices so that unsubsidized plants can cease to be viable economically. In particular, where intermittent renewable sources dump their surplus electricity on neighbouring transmission systems they undermine load factors for incumbent base-load providers. Many gas plants, even very new ones, have closed as a result and nuclear plants are also affected. However, there seems no disagreement that such conventional generation will remain a vital part of the EU energy mix for the foreseeable future.

Norway

In December 2024 Norway's two governing parties said they intended to end interconnection with the EU in 2026. A lack of wind in Germany and the North Sea in December 2024 pushed electricity prices in southern Norway to their highest levels since 2009.

Nuclear energy cooperation in the EU

Cooperation within Europe and between Europe and third countries operates at several different levels. The European Atomic Energy Community (EURATOM) was established by one of the Treaties of Rome in 1958 to form a common market for the development of the peaceful uses of atomic energy. It initially comprised Belgium, France, West Germany, Italy, Luxembourg, and The Netherlands at a time when energy security was a prime concern. The Treaty originally envisaged common EU ownership of nuclear materials. Politically it was both a counter to US dominance and a means of cooperation with the USA by providing guarantees of peaceful use, being the basis of the first multilateral safeguards system preceding the Nuclear Non-Proliferation Treaty (NPT). It now includes all European Union (EU) members, but remains legally separate from the EU.

The Euratom Treaty provided a stable legal framework that encouraged the growth and development of the nuclear industry while enhancing security of fuel supply for it and nuclear plant safety. It covers all civil nuclear activities in the European Union and aims to provide a common market in nuclear materials, to ensure nuclear fuel supplies, and to guarantee that nuclear materials are not diverted from their intended purpose.

Euratom has signed bilateral co-operation agreements to ease trade with its major partners. It also operates a comprehensive regional system of safeguards designed to ensure that materials declared for peaceful use are not diverted to military use. Today Euratom in its own right is a member of the Generation IV International Forum and the ITER consortium building a fusion reactor. It has remained substantially unchanged and is largely independent of EU parliament's control – a point of criticism of it. Euratom funding for 2012-13 was €118 million for fission research including radiation protection and €233 million for nuclear research at the EC’s Joint Research Centre, as well as over €2.2 billion for ITER fusion project.

The European Nuclear Education Network is a programme which promotes educational and research collaboration across Europe. It allows students to earn credits in a nuclear discipline outside of their host country to gain the extra qualification of the European Master of Science in Nuclear Engineering. EU funding for nuclear-related subjects in universities is spread across education and research projects which develop partnerships among many European universities and organizations, especially regarding European nuclear research projects funded by Horizon 2020. The University of Manchester helped define the mission of the EU Sustainable Nuclear Energy Technology Platform (SNETP), which was launched in 2007, and the UK aims to maintain its educational links with the rest of Europe beyond 2018.

In March 2013, 12 EU states joined together to promote the role of nuclear energy in the EU’s energy mix. The countries that signed the agreement are the UK, Bulgaria, Czech Republic, Finland, France, Hungary, Lithuania, the Netherlands, Poland, Romania, Slovakia and Spain. The Czech Republic is coordinating this group. A joint statement said that they are "committed to collaboration on safety and creating greater certainty for investors in low-carbon infrastructure projects." They pledged to press ahead with the deployment of low-carbon technologies, including nuclear power, renewable energy, and carbon capture and storage. In addition to the joint statement, the UK and France pledged to invest £12.5 million in funding for the 100 MWt Jules Horowitz research reactor being built in France. This is a €500 million project, half funded by France’s CEA and 20% by EU research institutes.

In July 2014 a letter to the EC on behalf of nine of these countries plus Slovenia demanded a level playing field for nuclear power among other low-emission sources in the EU so that it could play a greater role in energy security, sustainability and emissions reduction. “In our view, nuclear energy, for its physical and economic characteristics, is entitled to be treated as an indigenous source of energy with respect to energy security, having an important social and economic dimension... It is important that the market failures and the need to hedge against investment risks are accounted for in order to create the necessary market conditions for investment in new nuclear build projects in Europe. A technology neutral approach creating a level playing field for all low-emission sources is crucial.”

In Eastern Europe, consideration of future options involves the contiguous Visegrad group countries within the EU – Poland, Slovakia, the Czech Republic and Hungary. These are cooperating closely on nuclear power issues, including in research into future reactor designs and infrastructure development. They are all keen to reduce reliance on Russian gas imports. The Visegrad alliance was established in 1991 and its members became part of the EU in 2004, though the name reflects a similar alliance from 1335 set up in the Hungarian town of that name.

The EU’s Sustainable Nuclear Energy Technology Platform (SNETP) agreed by member countries, is structured around three main pillars: NUGENIA, to develop R&D supporting safe, reliable, and competitive GEN-II and GEN- III nuclear systems; the Nuclear Cogeneration Industrial Initiative (NC2I) for the low-carbon cogeneration of process heat and electricity based on nuclear energy; and the European Sustainable Nuclear Industrial Initiative (ESNII) which promotes advanced Fast Reactors with the objective of resource preservation, plutonium management, and minimizing the burden of radioactive wastes. ESNII is focused on three technology streams: SFR Astrid, LFR Myrrha and Alfred, and GFR Allegro (see Fast Neutron Reactors paper).

Energy co-operation and integration of energy networks is developing rapidly, both within the EU and between East and West Europe. The framework for such developments includes the European Energy Charter, the Energy Charter Treaty (ECT), and the Trans-European Energy Networks (TENs). The Synergy program governs the Community's general energy relations with third countries.

In 1991 EDF from France, Nuclear Electric from UK, UNESA from Spain, Vereiningung Deutscher Elektrizitätswerke from Germany and Tractebel from Belgium started a collaboration to produce standardized European Utility Requirements for light water reactors. The EUR organization today includes 17 European utilities that might build new Generation III plants in the future (CEZ, EDF Energy, EDF, Endesa, EnergoAtom, Fortum, Gen Energija, Iberdola, MVM, NRG, RosEnergoAtom, SOGIN, Swissnuclear, GDF-Suez/Tractebel Engineering, TVO, Vattenfall, VGB Powertech). The specified common requirements serve as an important guide within Europe and beyond.

In September 2025 the European Industrial Alliance on SMRs adopted its first Strategic Action Plan outlining 10 measures to rebuild the supply chain, support demonstration projects, and accelerate permitting and financing to enable SMR deployment in Europe by the early 2030s.

European regulation and safety

The principal responsibility for regulation and safety of nuclear facilities is with national authorities, and this independence is strenuously guarded against EU encroachment. An EC nuclear safety directive in 2009 emphasised the fundamental principle of national responsibility for nuclear safety. An amendment to the safety directive approved by the EC in July 2014 introduces a high-level EU-wide nuclear safety objective that aims to limit the consequences of a potential nuclear accident as well as address the safety of the entire lifecycle of nuclear installations (siting, design, construction, commissioning, operation and decommissioning of nuclear plants), including on-site emergency preparedness and response. It also introduces a set of rules to support the independence of national nuclear safety regulators, with a new peer review system.

The EU industry association Foratom said the directive "strengthens the role and independence of Europe's national regulators and endorses agreed safety objectives for nuclear power plants, in accordance with the recommendations of the Western European Nuclear Regulators' Association (WENRA)." Controversial proposals to develop harmonized safety guidelines and an EU-wide licensing process did not make the final text.

A less controversial directive on waste management was adopted in July 2011. This requires member states to develop national programs detailing where and how they will construct and manage final repositories. The first report on the implementation of this directive is to be submitted in August 2015, then every three years thereafter.

Two associations of regulators are important – WENRA and ENSREG – and they became more significant after the Fukushima accident.

The Western European Nuclear Regulators' Association (WENRA) is a network of chief regulators of EU countries with nuclear power plants and Switzerland, with membership from 17 countries. Other interested European countries have observer status. It was formed in 1999 and has played a major role in coordinating safety standards across Europe including significant involvement in Eastern Europe. It is seeking increasing engagement with regulators in Armenia, Ukraine and Russia.

In Europe, six national agencies from the EU have combined to form a group to assist Eastern European countries with radioactive waste management.

The European Nuclear Safety Regulators Group (ENSREG) is an independent, authoritative expert body created in 2007 by the European Commission to revive the EU nuclear safety directive, which was passed in June 2009. It comprises senior officials from the national nuclear safety, radioactive waste safety and radiation protection regulatory authorities from all EU member states, and representatives of the European Commission. Its role is to help to establish the conditions for continuous improvement and to reach a common understanding in the areas of nuclear safety and radioactive waste management. It continues to make recommendations to and through the European Commission.

The national progress reports on European stress tests in 2011 are published by ENSREG.

Early in 2010 four national technical safety organizations set up a European Nuclear Safety Training and Tutoring Institute (ENSTTI) to help strengthen European research and assessment in the fields of nuclear safety and radiation protection. The institute is a joint initiative of France's Institut de Radioprotection et de Sûreté Nucléaire (Institute for Radiological Protection and Nuclear Safety, IRSN); Germany's Gesellschaft für Anlagen- und Reaktorsicherheit (GRS); the Nuclear Research Institute Rez (UJV) of the Czech Republic; and the Lithuanian Energy Institute (LEI).

The European Bank for Reconstruction and Development (EBRD) was founded in 1991 to be an international development bank for former communist countries, though its remit was extended to Turkey in 2009 and some MENA countries in 2012. It administers three funds for nuclear safety on behalf of the G24 countries and the EU for which €1.5 billion has been pledged: the Nuclear Safety Account (NSA); the International Decommissioning Support Funds (IDSFs) for Bulgaria, Lithuania and the Slovak Republic; and the Chernobyl Shelter Fund (CSF). The EBRD provides technical, financial, legal and administrative services.

At their Munich Summit in July 1992, the G7 countries initiated a multilateral program of action to improve nuclear power plant safety in Eastern Europe, including some countries which have since joined the EU. In February 1993 the G7 officially proposed that the EBRD set up a Nuclear Safety Account, to receive contributions by donor countries to be used for grants for safety projects. The first four projects financed safety upgrades for Bulgaria's Kozloduy plant, Lithuania's Ignalina plant, Russia's Leningrad, Novovoronezh and Kola plants and for Chernobyl in Ukraine. However, the continuing concerns following the Chernobyl accident over two types of Russian nuclear power reactors in Eastern Europe led to the EU requiring that these be shut down as part of EU accession negotiations with the countries hosting them. Eight reactors were involved over 2002-09: six VVER-440/V-213 models in Bulgaria and Slovakia, and two RBMK reactors in Lithuania. See also: Early Soviet Reactors & EU Accession paper.

In November 2013 the European Parliament backed a €631 million program over 2014-20 to support nuclear safety in countries aspiring to join the EU, or in neighbouring EU countries. This continues from a similar 2007-13 program.

The Nuclear Safety Assistance Coordination Centre database lists Western aid totalling almost US$1 billion to more than 700 safety-related projects in former Eastern Bloc countries.

The EU also supports nuclear safety through various agencies and programmes such the TACIS (CIS states) and PHARE (East Europe including the Baltic states) programs and various funds. In addition, the European Investment Bank (EIB), the financing arm of the EU, administers a US $1.4 billion long-term loan facility for Euratom to fund nuclear safety projects in eastern Europe, in particular those related to later-model VVER reactors. Further funding comes from the European Commission’s Directorate General for Transport and Energy which also has a direct responsibility for nuclear safety.

In September 2025 the EAGLES-300 consortium signed an agreement with regulators from Belgium, Italy, and Romania to launch an international pre-licensing initiative for its lead-cooled SMR, aiming to harmonize safety requirements, streamline approvals, and commercialize the design by 2039.

Uranium supplies for the EU

Euratom reported that in 2021, 11,975 tonnes of uranium was delivered to EU-27 utilities. This represented about one-quarter of world supply from mines. Nearly all of this (96%) was under long-term contracts. In addition, MOX fuel containing 4.9 tonnes of plutonium was used, representing a saving of 439 tonnes of natural uranium and 0.31 million SWU.

The main sources of 2021 uranium deliveries were: Niger 24%, Kazakhstan 23%, Russia 20%, Australia 16%, and Canada 14%. The 2021 average price for deliveries under long-term contracts was €89/kgU, 24% higher than in 2020. In 2021 enrichment was supplied by: EU (Orano and Urenco), 6.39 million SWU; Russia (Tenex), 3.19 million SWU; and others, 0.71 million SWU.

At the end of 2021 inventories declined to 36,810 tonnes of natural uranium equivalent, down about 25% since the end of 2017.

Euratom reported that in 2021, 2197 tU of fresh fuel was loaded into commercial reactors in the EU-27. It was produced using 15,401 tU of natural uranium and 183 tU of reprocessed uranium as feed, enriched with 11.59 million SWU. In 2021, the fuel loaded into EU reactors had an average enrichment of 4.11% and an average tails assay of 0.22%.

Notes & references

General sources

New Nuclear in Europe – 2030 outlook, World Nuclear Association, ISBN 9780955078484 (July 2014)

Development And Integration Of Renewable Energy: Lessons Learned From Germany, FAA Financial Advisory AG (Finadvice), July 2014

Euratom Supply Agency Annual Reports

Fraunhofer IWES, The European Power System in 2030: Flexibility Challenges and Integration Benefits – An Analysis with a Focus on the Pentalateral Energy Forum Region (June 2015). Analysis on behalf of Agora Energiewende

Technical And Economic Analysis Of The European Electricity System With 60% RES, Alain Burtin, Vera Silva, EDF Research and Development Division (June 2015)

Security alert: Europe needs more grids, more power plants, Energy Post (17 November 2015)

Gerard Wynn and Paolo Coghe, Institute for Energy Economics and Financial Analysis, Europe's Coal-Fired Power Plants: Rough Times Ahead (May 2017)

Related information

BelgiumBulgaria

Czech Republic

Denmark

Finland

France

Germany

Hungary

Italy

Lithuania

Netherlands

Poland

Romania

Slovakia

Slovenia

Spain

Sweden

Switzerland

United Kingdom